0208 561 2112 (London) 0131 333 2700 (Edinburgh)

Quick Quote

- Private hire

- Corporate hire

- Tour operators

- Schools and colleges

- Contract hire

- Contingency hire

- Dedicated staff travel service

- West London

- Coach servicing

- Why choose us

- Our London team

- Our Edinburgh team

- Customer charter

- Environment

- Accreditations

- Driver training

- Areas Covered

Is there VAT on coach travel?

We commonly hear the term VAT being thrown around throughout daily life, whether we be at work, doing our weekly shop or out in public, but what is VAT and when does it apply?

What is VAT?

Value Added Tax (VAT) is added to the majority of goods, products and services throughout the European Union and the United Kingdom at a value of 20%. This 20% then gets submitted to the government as a form of tax. However, there are a minority of goods and public services which are exempt from VAT, and others that are listed as zero-rated.

What is the difference between exempt and zero-rated?

Exempt and zero-rated are preferential statuses given by the government for certain essential goods and services.

Companies who supply zero-rated products are still able to reclaim their input VAT, even though they don’t add value added tax to their goods. This is because the product is still taxable, but the rate is 0%.

Companies who supply services and goods which are listed as exempt are not VAT registered. There is no value of VAT added to these products and so there is nothing to reclaim.

Coach travel is listed as a zero-rated essential service, meaning that there should be no VAT charge when travelling via coach. However, additional extras, such as catering or entertainment services in action whilst on board are VAT registered and you will be expected to pay the additional charge of 20% for these services. This is the same amongst all other forms of domestic passenger transport which can be used to carry 10 or more people at a time.

If you would like to find out more about the costs of coach travel with City Circle , get in touch with our friendly bookings team who will be happy to assist and advise you in regard to any future bookings. Whether you are based in the UK or Scotland, we have a happy and helpful team waiting to assist you with any coach travel queries. Call our London branch on 020 8561 2112 or our Edinburgh branch on 0131 333 2700 . You can also email us at [email protected] and we will respond to your query within 24 hours.

Contact City Circle

Contact City Circle and discuss your requirements with our team to shape your perfect journey.

0208 561 2112

0131 333 2700

Your guide to VAT on travel

Table of Contents

What can I claim VAT on?

Can i reclaim vat on all types of travel, what if i use the flat-rate vat scheme, can i always claim 20% back, how to reclaim vat in 3 steps, step 1: register your business for vat, details you’ll need to provide, step 2: track your income and expenses, step 3: file your vat return and pay hmrc, how to pay hmrc, how to simplify your vat expenses with countingup.

Online conference calls don’t always cut it, and sometimes, businesses need to expense travel costs to meet clients or to make sure projects are delivered on time. Find out how you can claim VAT back on your travel costs in this article.

We’ll summarise the essential information you’ll need to successfully make a VAT claim from your travel costs and answer key questions, including:

- What if I use flat-rate expenses?

Growing a successful business on the go means identifying ways you can save time and effort to focus on what matters. Learn how you can simplify your VAT expenses with Countingup below.

Businesses can reclaim VAT costs from the goods and services they purchase for business purposes, including things like travel costs. For this reason, only VAT claims on travel that’s related to your business are allowed. HMRC may audit your business

For example, if you need to provide a quote on a client project and have travelled to their home or offices to do so, your business is typically able to claim costs like VAT on travel back. Similarly, if you travel to attend a trade show or meet with potential investors or lenders, you can reclaim any VAT you’ve paid. Additionally, if you expand your business to a new location and need to travel in order to establish it, HMRC allows expense claims to be made for the first 24 months.

However, if you travel to the same office or manufacturing location regularly, this type of travel can’t be claimed back as it’s part of your normal commute. Moreover, if you exceed this 24-month threshold, you may lose your ability to claim the VAT back. This is because HMRC allows business travel for limited durations or for temporary purposes. If you’d like to learn more about the policy HMRC has for travel expenses, you can read our article What is the HMRC 24-month rule for expenses?

Yes, businesses can claim expenses on all types of travel, including any VAT rates that have been applied. However, if you choose to travel by car, expenses are handled differently. This means that if you travel by plane, train or bus, you can claim the ticket cost and other associated fees.

However, if you drive your own car, you can claim VAT in three different ways . In general, it’s simpler to file your car expenses under the Flat Rate VAT scheme (see below) as it includes VAT expenses on other vehicle costs like MOT and usage. If you’d like to learn more about how to handle your VAT costs, use the links provided above or speak with your accountant.

If your business has signed up for the Flat Rate VAT scheme , your VAT returns will be handled slightly differently.

The Flat Rate VAT scheme aims at helping businesses simplify their VAT payments to HMRC, by allowing them to keep the difference between the fixed VAT rate paid to HMRC and what they’ve charged to customers. However, the scheme places a minimum value on expenses you can claim VAT on.

Businesses are only able to reclaim the amount of VAT applied to the goods and services they’ve been charged for. This means that you can’t claim a consistent 20% across all the goods you’ve purchased – only the amount of VAT applied to each of them.

For example, most travel costs are charged at the standard 20% rate. However, if you happen to buy food while you’ve travelled, most items are exempt . If you don’t use the Flat Rate VAT scheme for your vehicle, VAT claims on fuel are calculated using the fuel scale charge. You can work out how much your vehicle is eligible to claim on VAT costs using HMRC’s online tool .

Reclaiming VAT costs works similarly to other expenses your business has, however, there is an additional step you’ll need to take – namely registering for VAT in the first place. We discuss the process for how you can reclaim your VAT below in three simple steps.

In order to be eligible to reclaim VAT, your business needs to be VAT registered also. Businesses can register for VAT with HMRC using the online portal . This process will create a VAT online account (sometimes referred to as a ‘Government Gateway account’) which you can use to submit your VAT returns each year.

Businesses need to register if their VAT-taxable turnover is over £85,000. This means that if your turnover is less than this amount, you may not need to register. However, if you know your turnover will pass this threshold in the next 30 days, or if your turnover from the last 12 months has already passed it, HMRC requires you to register for VAT. If you’d like more information on whether you need to register for VAT, read our article When do you pay VAT?

Note that, some businesses may have to register by post using the VAT1 form. For example, if you’re applying for a registration exception (if you sell goods completely exempt from VAT charges) or are joining the Agricultural Flat Rate Scheme (if your business is in agriculture, you may be eligible for a flat tax rate). Similarly, if you import goods to Northern Ireland worth more than £85,000 from an EU country (like the Republic of Ireland), you should register for VAT by post using VAT1B .

Regardless of which method you use to register, you’ll need to provide details about your business to HMRC during the process. These will include your business’ turnover , bank details, what it does to make a profit.

This information helps HMRC understand if your future VAT returns are correct (as you may exclude certain items from your VAT calculations across the year). If you haven’t already, it may be useful to have a dedicated bank account for your business as it can help your VAT calculations be more accurate and transparent.

If you sell goods across the UK to Northern Ireland, you may have to provide additional details to HMRC. In these cases, you need to tell HMRC if any of the following apply:

- Your goods are in Northern Ireland at the time of sale

- You receive goods in Northern Ireland from VAT-registered EU businesses for any business purposes

- You sell or transport goods from Northern Ireland to an EU country

This is to help your business use simplified VAT rates when trading with EU customers or businesses. For more information on the registration process, read our article How to register for VAT .

Businesses are required to keep records of their sales and expenses in order to calculate their taxes accurately, and VAT is no different.

Once you’ve registered, you’ll need to correctly apply VAT rates across your goods and services, and keep receipts of expenses where you’ve been charged VAT in order to claim it back. Without this accurate record, you may over-pay on your VAT return to HMRC.

Even if you have an organised and thorough system of recordkeeping, it still takes a significant amount of time to maintain across the financial year. Learn about how you can ease this burden below.

VAT returns are typically due every three months. VAT returns can be completed online or using integrated accounting software like Countingup if you’ve signed up for Making Tax Digital for VAT .

The specific steps for completing your VAT return will vary depending on which scheme you’re on. For example, whether you’re a part of the Flat Rate , Retail , Agricultural Rate , or any other VAT schemes. Similarly, VAT returns for businesses registered in Northern Ireland need to include an EC sales list as part of their submission.

HMRC has guidance published for how to file and submit your VAT return available here .

HMRC accepts several different payment methods in order to help businesses pay their required VAT amounts easily. These include:

- Online and in-person money transfers from banks or building societies

- Direct debits and standing orders

- Debit or corporate credit card payments

You’ll need to have crucial pieces of information ready, including your VAT registration number (which you would have received when you first registered) and the correct VAT sum.

Depending on the method you use, it could take up to six weeks to successfully complete the entire payment process – which is why it’s vital to plan ahead and be prepared. If you’d like more information on how to pay HMRC and what happens if you’re late, read our articles How to pay VAT to HMRC and What happens if you don’t pay VAT on time?

Tracking VAT rates across your business’ accounts can be a time-consuming and frustrating chore that distracts you from building your business. You can use the Countingup app to save time and stress on your financial admin.

Countingup is the business current account and accounting software in one app and provides a digital tax filing service to small businesses. With it, you can automate VAT calculations associated with each of your business transactions and make paying your VAT bill easier. If you’re new to the world of business, Countingup also makes it easier to share your business’ finances and VAT records with your accountant. With the touch of a button, you can send your transaction data for review so you can make sure you’re always compliant.

The Countingup app also offers essential business tools to save you time, including automated invoicing features and a receipt capture tool that can log expense and VAT data even while on the go. Best of all, Countingup offers you real-time profit and loss statements so you can make sure your insight is always up to date and accurate.

Make logging your VAT costs while travelling easier and more straightforward. Find out more about Countingup here and sign up for free today.

- Counting Up on Facebook

- Counting Up on Twitter

- Counting Up on LinkedIn

Related Resources

What insurance does a self-employed hairdresser need.

As a self-employed hairdresser, you’re open to risks in your everyday work. Whether

What are assets and liabilities in a business?

Anyone going into business needs to be familiar with assets and liabilities. They

Personal car for business use: How does it work?

Access to a car is a must for most businesses, meaning that travel

Advantages and disadvantages of using personal savings in business

Have you got a new business idea? And are you considering using your

How to pay Corporation Tax

Corporation Tax is the main tax your limited company has to pay every

How long do CHAPS & BACS payments take?

If you are making transfers frequently between banks in the UK, you have

11 common costs of running a business

When running a business, the various costs can quickly add up. If you

How to buy a vehicle through a limited company

Buying a vehicle through a limited company works similarly to how you may

What is a sales strategy? (with example)

When you run a small business, it’s important to consider how you’ll optimise

Preparing business packages for distribution

You may think shipping your product is as easy as popping it in

How to use cloud services for a business

The development of cloud computing is a game changer for businesses big and

How do EU imports and exports work?

In January 2022, the UK introduced new EU imports and exports regulations. If

You are here

- Are the travel services still to be treated as a single bundle of services? If so, would the bundle in B2C cases be deemed to have been provided where the supplier is established in accordance with sec. 3a para. 1 UStG? And in B2B cases according to sec. 3a para. 2 UStG, where the recipient of the service is established?

- for accommodation, where the property is located (sec. 3a para. 3 no. 1 sentence 2 letter a UStG)

- for catering services, where the catering takes place (sec. 3a para. 3 no. 3 letter b UStG)

- for passenger transport services where the transport takes place (section 3b subsection 1 UStG)

- for tour guide services where supplier or recipient is established (sec. 3a para. 1 or 2 UStG)

- Which VAT rate is applicable? Does the reduced VAT rate apply, e.g. temporarily for catering services?

- In B2B cases, is the VAT liability shifted to the customer in the country of travel (Germany)?

- For which input services rendered by subcontractors not resident in Germany may the VAT liability be shifted to the recipient according to sec. 13b UStG? In this instance there would be a corresponding input VAT deduction, i.e. no loss of liquidity, but a registration obligation in Germany.

- Could double taxation of the services rendered occur due to taxation in both the country of residence and the country of travel (Germany)?

- Could an advantage arise because the services are deemed to have been rendered in the country of residence according to sec. 3a para. 1 UStG, but no taxation takes place there according to local regulations (double non-taxation), while an input VAT refund is possible from services purchased in Germany (e.g. hotels)?

- Can the One-Stop Shop procedure be used for the declaration? Then input VAT would have to be applied for reimbursement in the 13th Directive refund procedure, with processing times usually exceeding one year. Would the regular submission of VAT returns therefore be more advantageous?

- Or are services received for which the VAT liability is shifted, in which case the One-Stop Shop procedure would not be applicable? Input VAT could then only be claimed by filing VAT returns after a VAT registration.

Ronny Langer Certified Tax Consultant, Dipl.-Finanzwirt (FH) Phone: +49 89 217501250 [email protected]

As per: 04.02.2021

Data protection

This website uses cookies to ensure the correct functionality of the site. Cookies are also set to measure website traffic and the conversion rate of LinkedIn campaigns on this site. For this purpose, your IP address is sent to the services of Google Analytics & LinkedIn. If you agree, personal data will be processed for the following purpose: to measure the number of visits to this page. If you do not agree, cookies will only be set to ensure the functionality of the website.

You are currently viewing our [Locale] site

For information more relevant to your location, select a region from the drop down and press continue.

Is there VAT on train tickets? (and other common VAT questions)

VAT: what can you claim?

VAT is a tax charged on a range of goods and services that can be purchased for use by a business. If your business is registered for VAT , you can often reclaim this tax as a refund from HMRC by filing a VAT return .

VAT is charged at different rates for different products and services and you can only reclaim what you pay for. Most of the time this means you can reclaim VAT at the standard rate (20% of the cost of the product or service) or at the reduced rate (5%). However, while VAT technically exists on zero-rated products it is charged at 0% - so you don’t pay anything extra and as a result can’t claim anything back!

VAT is one of the most complicated areas of the UK tax system and as a small business owner you might often be left scratching your head over what items are exempt from VAT and what you can claim back. If you’re struggling to figure out what goods and services are exempt from VAT (and therefore what you can and can’t claim VAT back on), this guide will help.

Jump to a section or read on to learn more:

1. Can you claim VAT back on travel?

2. Can you claim VAT back on food and drink?

3. Can you claim VAT back on property?

4. Other common VAT questions

Can you claim VAT back on travel?

Train tickets.

No - train tickets are zero-rated for VAT so you can’t claim anything back.

No - like train tickets and most public transport costs, bus fares are zero-rated for VAT so you can’t reclaim anything on them.

Yes - you can usually claim VAT on taxi fares at the standard rate (20%) unless the taxi driver is self-employed and not registered for VAT - always ask for a VAT receipt. It’s worth noting that the majority of Uber drivers are self-employed and earn under the VAT threshold, so you can’t usually reclaim VAT on Uber fares.

Fuel and mileage

Yes - VAT is charged and can usually be claimed on petrol and diesel at the standard rate of 20% for business travel. If your accounts come under investigation from HMRC , you may be asked to provide a travel log to prove the journey was business related. The log should include:

- where the journey started and ended, including postcodes

- who you visited and why

- the date of the journey

Mileage for business journeys can also be claimed as an expense; you can find out more in our guide to motor expenses . If you’re claiming a mileage allowance rather than the actual costs of your journey, you can only reclaim VAT on the fuel element of the mileage allowance.

Flights/air travel

No - air travel is zero-rated for VAT so you can’t claim anything back.

Car parking

Maybe - street parking is exempt from VAT so you can’t claim back VAT on charges from a parking meter. Private car parks, however, may charge VAT if the car park business is VAT-registered, so you should always check your receipt for a VAT number. If there’s a VAT number on your receipt you should be able to reclaim VAT on parking charges.

Car hire/leasing

Yes - if you hire or lease a car then you can usually reclaim at least 50% of the VAT on the hire fees. You may be able to reclaim 100% of the VAT charge if the car is only used for business purposes and is not available for private use.

Commercial vehicles/company cars

Maybe - you can sometimes reclaim the VAT for buying a car if you use it exclusively for business purposes. HMRC is strict about this, so reclaiming VAT on a car can be a challenge unless in certain circumstances, such as for a taxi or a driving school car. VAT is charged at the standard rate of 20% for almost all new cars and vehicles but this rate may differ for second-hand purchases (see below).

You may also be able to reclaim VAT on a commercial vehicle if it is used exclusively for business purposes. Commercial vehicles include tractors, vans and lorries but you may also be able to reclaim VAT on motorcycles, motorhomes, combi vans and car-derived vans if they are used entirely for business purposes.

Congestion charge

No - as statutory fees, such as the London congestion charge, are outside the scope of UK VAT, you cannot reclaim VAT on them.

Vehicle insurance

No - vehicle insurance is exempt from VAT so you can’t claim anything back.

Second-hand cars

Maybe - cars that are bought and sold privately (i.e. by anyone outside the motor trade), are outside the scope of VAT. However, if a car is bought from a VAT-registered dealership then the tax may apply. The rate of VAT applied may vary due to The Margin Scheme , so it’s important to check your receipt to see how much you’ve been charged.

Maybe - MOTs are outside the scope of VAT, provided that the cost does not exceed the statutory maximum. Any costs over and above the statutory maximum should be expected to be standard-rated for VAT.

Vehicle road tax

No - UK road tax is outside the scope of VAT.

Can you claim VAT back on food and drink?

Maybe - a jar of coffee bought from a shop is zero-rated for VAT, so you can’t claim anything back. However, coffee that is bought as a hot beverage (i.e. from a cafe, restaurant or takeaway) is standard rated at 20%, but you can’t reclaim this VAT if you bought the coffee for the purpose of business entertaining .

No - milk (including soya, rice and coconut milk) is zero-rated for VAT, therefore you can’t claim anything back. This also extends to flavoured milk drinks, including milkshakes.

No - cakes are zero-rated for VAT, therefore you can’t claim anything back. Even if a cake is still warm when it’s sold, it remains zero-rated as it’s not sold with the intention of being eaten hot. If you go ahead and eat it before it cools we promise not to tell!

Bottled water

Yes - bottled water is taxed at the standard rate of 20% for VAT.

Maybe - biscuits are zero-rated for VAT unless they are wholly or partially coated in chocolate, in which case they are charged at the standard rate of 20%.

Yes - chocolate bars, including diabetic chocolate, are standard-rated for VAT at 20%.

Yes - alcoholic beverages (including beer, cider, wine, spirits and liqueurs) are standard-rated for VAT at 20%. Again beware that you can’t reclaim VAT on alcohol bought for the purpose of business entertaining .

Maybe - shop-bought sandwiches, such as those sold in supermarkets, are zero-rated for VAT, so you can’t claim anything back.

Cold sandwiches bought in an eatery such as a cafe or sandwich outlet are zero-rated if they are not consumed on the premises. However, they are charged at the standard rate of 20% if they are consumed on the premises. This is why ‘eat-in’ and ‘takeaway’ prices often differ in cafes.

Hot sandwiches are charged at the standard rate of 20% wherever you choose to eat them.

Restaurant food

Maybe - food purchased and consumed in a restaurant is usually charged at the standard rate of VAT (20%) regardless of whether it’s hot or cold. One exception to this rule is if you buy cold food from a restaurant but don’t eat it on the premises. Again beware that you can’t reclaim VAT on meals bought for the purpose of business entertaining .

Reclaiming VAT on food and drink

In order to claim any VAT on food and drink, HMRC will have to be satisfied that it qualifies as a reasonable business cost - which can be tricky! Our guide to claiming expenses for the cost of food and drink has more information on this topic, but it’s always wise to check with your accountant before claiming any tax.

Can you claim VAT back on property?

Vat on building work and renovations.

Maybe - VAT for most work on houses and flats by builders, plumbers, plasterers, carpenters and similar trades is charged at the standard rate of 20%.

However, building work for a new home or for aiding people with disabilities may be zero-rated for VAT.

Building a new home

Maybe - when building a new home, VAT is likely to be charged on the supply of materials only. However the supply of labour or the joint supply of labour and materials is likely to be zero-rated, so you won’t be able to claim anything back.

You can apply to HMRC for a VAT refund on building materials if you are building a new home or converting an existing non-residential property into a home. This also applies to non-profit communal residences such as hospices. You must apply to HMRC for this refund within three months of completing the work to be eligible.

Estate agent fees

Yes - estate agent fees are charged at the standard rate of 20%. Can you claim VAT on amenities?

Maybe - water supplied to households and most premises is zero-rated for VAT, so you can’t claim anything back. Some businesses in the manufacturing, construction and engineering sectors may be required to pay VAT at the standard rate of 20% for water.

Electricity bills

Yes - VAT is charged at the reduced rate of 5% for the supply of electricity to domestic properties or for non-business use by a charity. Electricity supply for business use is usually charged at the standard rate of 20%.

Yes - VAT is charged at the reduced rate of 5% for the supply of gas to domestic properties or for non-business use by a charity. Gas supply for business use is usually charged at the standard rate of 20%.

Other common VAT questions

Can you claim vat on insurance.

No - insurance is largely exempt from VAT and doesn’t incur any charges beyond Insurance Premium Tax (which is different from VAT), so you can’t claim anything back.

Can you reclaim VAT for bad debts?

Yes - you can reclaim the VAT that you’ve paid HMRC but have not received from a customer if it’s a ‘bad debt’ (i.e. one you do not expect to be paid). To qualify for the relief:

- the debt must be between six and 54 months old

- you must not have sold the debt on

- you must not have charged more than the normal price for the invoice item on which the debt has been incurred

Can you claim VAT on newspapers?

No - newspapers are zero-rated for VAT so you can’t claim anything back.

Can you claim VAT on sales to non-EU countries?

No - VAT is a tax on goods used in the EU. If goods are exported outside the EU they are zero-rated for VAT.

Can you claim VAT on charitable donations?

No - voluntary donations to charity are outside the scope of UK VAT, so you can’t claim anything back.

Can you claim VAT on stationery?

Yes - stationery is usually standard-rated for VAT at 20%.

Can you claim VAT on batteries?

Yes - batteries are usually charged at the standard rate of 20%. Certain batteries can be charged at the reduced rate of 5% when sold alongside a solar photovoltaic system .

Accounting for VAT in FreeAgent

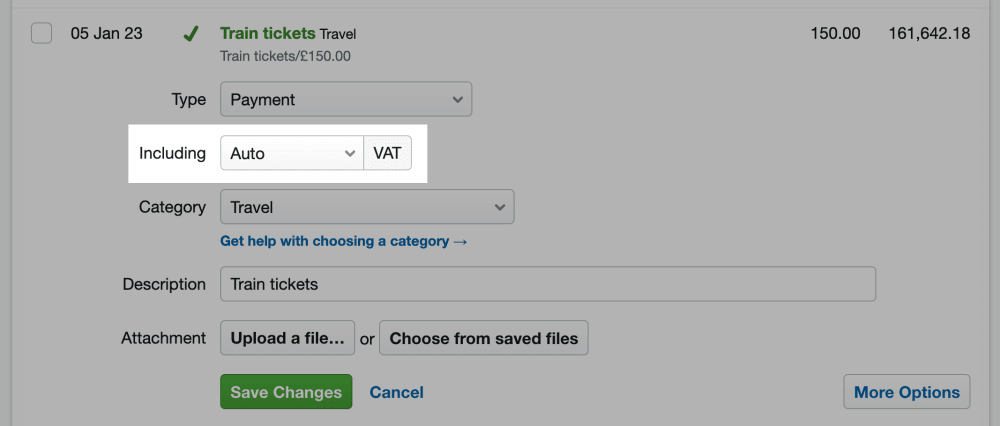

When explaining bank transactions in FreeAgent, you can select 'Auto' and the software will automatically apply the relevant rate of VAT for the category you're allocating the transaction to. This means that if you know a payment is for travel, you often don't have to worry about knowing the correct rate of VAT off the top of your head. If you do know the correct rate of VAT, you can also select this within the software!

Find out more about online VAT filing with FreeAgent.

Disclaimer: The content included in this guide is based on our understanding of tax law at the time of publication. It may be subject to change and may not be applicable to your circumstances, so should not be relied upon. You are responsible for complying with tax law and should seek independent advice if you require further information about the content included in this guide. If you don't have an accountant, take a look at our directory to find a FreeAgent Practice Partner based in your local area.

Say hello to FreeAgent!

Award-winning accounting software trusted by over 150,000 small businesses and freelancers.

FreeAgent makes it easy to manage your daily bookkeeping, get a complete view of your business finances and relax about tax.

Related articles

- What rate of VAT should you charge?

- The complete guide to charging and reclaiming VAT

Are you an accountant or bookkeeper?

The Pleo Blog

Looking for pleo.io ?

Tools & Tips

Is there VAT on train tickets? Don’t get derailed by hidden costs

Is there VAT on train tickets? Like all of life’s great questions, the answer is not as simple as it first appears. Value Added Tax rates on expenses such as train tickets and train travel is usually zero percent.

But there’s a big difference between zero-rated and being exempt from VAT taxation.

Keep reading to learn more about Value Added Tax on train travel, other forms of public transportation and how to account for VAT .

Content overview

Are train tickets subject to VAT in the UK?

Is there vat on public transportation in the uk, is there vat on other forms of transportation in the uk, how do vat refunds work for travel expenses, how to account for vat, pleo and train tickets a match made in heaven .

Train tickets in the UK fall under the zero-rated category. This means as a business you need to keep track of the 0% VAT you’re paying on train travel in your VAT returns.

This is different from being exempt from VAT. Unlike exempt items, like postage stamps , which the government considers as entirely outside the scope of VAT. The advantage of zero rating is that businesses can claim back VAT on related purchases, benefiting their cash flow , without having to charge their customers extra.

Reclaiming VAT on zero-rated supplies is what makes zero percent VAT such a favourable tax rate. You can claim all the benefits without the drawback of charging your customers extra.

Domestic UK transport is usually 0% VAT so long as the vehicle, ship or aircraft has at least ten seats, including those for the driver and crew.

This might look like:

- Pleasure cruises

- Cliff lifts

- Excursions by coach or train (including steam railways)

- Horse-drawn buses

- Mystery coach or boat trips

- Sightseeing tours

- The transport element of park-and-ride schemes designed to reduce traffic congestion in city centres

But there are some exceptions to this rule, which often focus on whether the transport you’re supplying is to an event, experience or entertainment that you also own. In which case you’ll need to charge the standard rate of VAT on the transport.

According to HMRC’s website , this would look like:

- Transport services when they’re included in the admission price to a place of entertainment, historic or cultural interest like a theme park or museum.

- The use of any vehicle to, from or within a place of entertainment, historic or cultural interest, if the transport and admission are supplied by the same or by connected persons

- Transport in any motor vehicle between a car park or its vicinity and an airport passenger terminal or its vicinity, when the car parking facilities are supplied by the same or connected persons

- Flights for entertainment or the experience of flying and not primarily to transport people from one place to another

Usually, passenger transport in a vehicle that can only accommodate less than ten passengers is subject to VAT at the standard rate . The standard rate of VAT in the UK is 20%.

More than ten seats: Probably zero-rated. Less than ten seats: Probably the standard rate. But let's take a closer look.

Is there VAT on Uber and taxis?

Yes, there is usually VAT on taxi fares at the standard rate unless the taxi driver is self-employed and not registered for VAT. So it’s always worth asking for a VAT receipt.

Bear in mind that most Uber drivers are self-employed and earn under the VAT threshold. So you’re less likely to get any sort of VAT return through Uber, whereas lots of taxi drivers work for larger firms that will have to charge VAT.

You’ll also be charged VAT on other parts of a taxi journey like:

- Waiting time

- Administration charges

If you give a tip to a taxi or Uber driver this is not regarded as payment for a supply, so is outside the scope of VAT.

Is there VAT on ferry travel?

So long as the ferry in question can carry more than ten people at a time, they are usually zero-rated for VAT purposes.

There is an exception to this rule for boat rides to, from, or within a place of entertainment or cultural interest. In these cases, the tickets are subject to standard-rate VAT rates. Ferries, canal boat trips, and similar boat excursions that do not have additional facilities and take place on the open sea or other waterways accessible to the public are zero-rated for VAT.

Is there VAT on buses?

VAT rates for buses are just like train tickets and other forms of public transport, zero-rated. Any travel expenses relating to a bus journey must be entered as zero-rated in your accounting software, and not exempt.

But remember in scenarios where the cost of bus fare is included with the right of admission to a place of entertainment or provided by the same provider then it is standard rate VAT.

Is there VAT on coaches?

Coach tickets do not have VAT added to their price because coach travel is considered an essential service that is zero-rated for VAT. However, certain things you buy during a coach journey, like onboard food and entertainment, may have VAT included in their cost.

Is there VAT on flights?

Public flights in the UK are VAT-free, so you don't have to pay or charge VAT on a flight ticket, but they’re not complete tax exemptions. You are subject to Air Passenger Duty (APD) that airlines include in the ticket pricing.

The amount of APD taxation depends on how far you're flying and the class you choose. Domestic flights are taxed for both the outbound and return trips, while international flights are only taxed on the outbound leg from the UK. Unlike VAT, you can't reclaim APD, except when you book a flight but end up not using it. In that case, you can reclaim the APD from the airline by filling out a form.

Private flights with less than ten passengers, or pleasure flights that are designed for an experience rather than transportation, are an exception and still subject to the standard 20% VAT rate.

Ultimately businesses claim all VAT refunds for travel expenses by completing the appropriate sections on their VAT return. If the amount of VAT you’re claiming exceeds the amount of VAT you owe, then the government will pay you back the difference in the form of a VAT refund.

In practice, this looks like:

- Making sure you’re VAT registered .

- Ensuring you have valid VAT invoices for all your postage expenses.

- Keeping accurate records of your input VAT.

- Filing your VAT returns on time and including postage costs.

You’ll then receive a VAT refund that includes VAT charged as part of travel expenses if you’ve shelled out more on VAT for things you’ve had to buy as a business, versus things you’ve sold as a business.

Remember that to be eligible for a refund you must meet all the necessary VAT compliance rules and regulations. HMRC may review your VAT refund claim, and request additional documentation or information to support your claim. So it's essential to maintain accurate records and be prepared to provide any relevant documentation.

If you register for VAT, there are a few different VAT accounting schemes you can use to go about telling the government how much you owe them and they owe you:

- Standard VAT accounting means you track purchases, sales, and VAT amounts, paying or claiming back based on invoice dates every quarter.

- The Flat Rate Scheme simplifies things, using a percentage of your annual turnover to calculate VAT.

- Cash Accounting is similar to standard VAT accounting but everything is based on the payment date, not the invoice date.

- Annual Accounting is for those who prefer filing VAT returns once a year and paying based on invoices.

What’s best for you and your business will depend on:

- Your cash flow

- How much VAT you pay out and get paid

- How large the finance team is in your organisation.

Managing expenses related to travel can be a hassle, especially when it comes to understanding and managing VAT. Pleo can help you:

- Centralise expense data

- Simplify expense reimbursement

- Automate receipts for Tfl journeys

Smarter spending for your business

Save time on tedious admin and make smarter business decisions for the future. Join Pleo today.

Powered in the UK by B4B partnership

Senior Content Manager

Content, demand gen and SEO professional. 5 years in the CPH start-up scene. Get in touch!

You might enjoy...

.png?ixlib=gatsbyFP&auto=compress%2Cformat&fit=max&dpr=2&w=373 "vat on coach travel")

The lowdown on professional subscriptions HMRC approves of in 2024

Find out which of your professional subscriptions HMRC approves of and how to get tax relief on them in 2024.

What businesses need to know about HMRC fuel rates for private cars in 2024

Businesses can offset fuel expenses for work-related journeys, but what about if you’re not driving a company car… can the fuel rates still...

What you need to know about HMRC uniform tax in the U.K. for 2024

Discover how you can turn time spent on washing your workwear into billable hours.

Get the Pleo Digest

Monthly insights, inspiration and best practices for forward-thinking teams who want to make smarter spending decisions

VAT and transport expenses: all you need to know

Magali Sire

Content manager

Updated on 07/08/2023

- Reclaim VAT

The travel costs of running a business can be substantial. This is true for companies of all sizes, from sole traders to multi-national corporations. The VAT regulations governing travel as well as ancillary costs such as accommodation , food and drink, road tolls, parking fees , corporate hospitality, entertaining clients and staff , and offering gifts are complex. It is worth finding out how and what you can reclaim . Find out all about VAT and how it applies to transport with Mooncard.

The provision of passenger transport services

The value-added tax ( VAT ) regulations on the provision of passenger transport services change regularly and it can be difficult for companies to keep up with developments. The latest UK notice on the supply of passenger transport services dates from January 2021. This notice, issued by the UK government, defines passenger transport services as being supplied when “a vehicle, ship or aircraft is provided together with a driver or crew, for the carriage of passengers”.

Passenger transport services include, for example , buses, coaches, trains, canal barges, taxis, ferries and so on, as long as they are provided with a driver. The VAT rate that can be applied to passenger transport services varies. They can either be zero - rated , reduced-rated or standard-rated.

The provision of a service to transport passengers within the UK can be zero-rated with regards to any vehicle, ship or aircraft designed to carry ten or more people, as well as any scheduled flight, and transport provided by the Post Office.

There are exceptions to this rule. These largely relate to the provision of transport to and from a place of entertainment if the same company is providing the transport and the entertainment.

Reduced-rate VAT applies to the provision of transport in the form of cable cars, gondolas and so on, as long as these vehicles are not designed to carry more than nine people.

The provision of taxi services, limousine services and hire cards is covered by the standard VAT rate (20%) unless the vehicle has ten or more seats.

VAT on different forms of transport

The amount of VAT that can be reclaimed on transport depends on the type of transport. Assuming that the purpose of the journey is “wholly and exclusively” connected to the business (visiting a customer , picking up supplies , attending a conference, for example), you may decide to use a number of transport options to complete the journey.

Although many companies now strive to reduce their air miles and use greener forms of transport, flights remain the only feasible option for many business trips, especially when time is of the essence. Domestic flights in the UK are zero-rated for VAT, so there is no VAT that can be claimed back .

The same holds for train tickets , which are also zero-rated for VAT. It is worth remembering that “zero-rated” is not the same as VAT-exempt.

One of the only forms of transport that VAT can be reclaimed on is taxis , but this is only the case if the taxi firm is VAT-registered. As with anything contained in your VAT return, VAT receipts must be provided, so remember to ask for one from the driver!

Finally, you or your employees may decide that it is most convenient to use a personal car to get to the destination, in which case mileage, fuel, and other costs such as parking can be declared as expenses and the VAT is deductible . If you decide to pay a mileage allowance to your staff, you should remember that only the fuel part of the allowance is VAT-deductible, not the part relating to wear and tear on the vehicle.

VAT on freight services

As with the provision of passenger transport services, the VAT regulations applying to the supply of freight transport are complex but worth understanding for companies involved in transporting goods .

The definition of “freight”, according to the UK government, includes the transport of goods or cargo, mail, documents and unaccompanied vehicles. “Freight transport services” are supplied when a vehicle is provided with a driver or crew for the purposes of carrying goods.

In terms of the VAT on freight services, this depends upon where the “place of supply” is. As with passenger transport, when the entire journey takes place within the UK, UK VAT regulations apply. The transport is, therefore, standard rated. Different rules apply when providing transport services between the UK and another country.

Transport outside the UK

If the transport takes place entirely within the UK, obviously the supplies are all considered as being inside the scope of application of the UK’s VAT regulations. However, specific VAT rules are applied to passenger transport that involves journeys that are partly within the UK and partly outside the UK. For example, a boat departing from an English port may transport passengers to Dublin and then return to the UK.

It is essential to determine where the “place of supply” is. In this case, the part of the journey that is within UK territorial waters is covered by UK VAT rules, while the remainder is not. One exception is cruise ships that enter the UK from abroad. These vehicles are considered to be outside the scope of UK VAT, as long as passengers neither embark for the first time nor definitively disembark while in the UK.

The VAT rules around transport, whether involving your staff, passengers or freight, are complex and it is worth finding out more about which rules apply to your situation. A Mooncard corporate card can help streamline your record-keeping and make it easier to file VAT returns and make claims. For more information , get in touch to book a no-strings-attached demonstration from Mooncard today!

Magali Sire is Marketing & Brand Content Manager at Mooncard. An entrepreneur and experienced copywriter, she has been a Swiss Army knife for over 20 years in BtoB and BtoC, research, economic and financial media and retail, and is passionate about the development of support professions.

Browse Help by Category

- Account and payments

VAT Invoice/Expense receipts

Trainline will provide you with a receipt for proof of payment and/or proof of travel, this is available from our app or website.

This receipt is not a VAT invoice for the total cost of your travel.

Trainline sells tickets to you on behalf of the Rail and Coach providers and do not charge VAT on your Rail and Coach travel, this is the responsibility of the Rail and Coach providers.

Where VAT is charged on Rail and Coach travel (usually within the EU), this will either be shown on your ticket or you can obtain an invoice directly from the Rail and Coach provider if you need to recover VAT for your business account.

Trainline does charge VAT on the booking fees applied, this is shown on your email conformation and the receipt available from the app or website, both can be used as a VAT receipt.

How do I get an expense receipt

A receipt for proof of payment and/or proof of travel is available from our App or website, following the directions below:

If using our website

- Login into My Bookings .

- Find the relevant booking under Upcoming or Past tab, click on " Order details and history" .

- An expense receipt/ invoice will be formatted ready for printing.

- Open ‘My tickets’ and find the relevant trip.

- Click ‘Manage my booking’ .

- Choose the option ‘Expense receipt’ .

- An expense receipt will be formatted ready for downloading.

You will require a trainline account to access My Bookings.

How do I get a VAT invoice?

Invoices with VAT number for your tickets, if available, are paid directly by the train operator.

Train Operators

All uk trains, deutsche bahn, öbb, ouigo spain.

Trainline sells tickets to you on behalf of the Rail and Coach providers and do not charge VAT on your Rail and Coach travel.

VAT on transport services is not deductible. SNCF do not issue invoices with a VAT number.

Deutsche Bahn and ÖBB do not issue invoices, but you can still find the details of the VAT applied directly on the ticket.

Invoices are issued directly by Trenitalia, available from midnight on the day of purchase at the latest. Visit ‘How to request an invoice during online purchase and ticket changes’ on Trenitalia's website.

Invoices are issued directly by Italo, available from midnight on the day of purchase at the latest. Visit Italo's website and enter your name and ticket reference to access the details.

You can request your invoice directly on the carrier website, by filling this form .

You can request your invoice directly on the carrier website , in "My bookings' section (page only in spanish).

Why am I paying VAT at different rates?

Trainline is required to charge VAT on our booking fee for the use of the Trainline app or website. The rate of VAT charged depends on the country you are travelling in. In the UK, VAT is 0% on Rail and Coach travel, this will show on your VAT receipt as UK VAT at 0%.

VAT rates vary between EU countries, to see the VAT rate for each EU member state click here .

Why have I paid for my ticket in one currency, but the VAT is showing another currency?

You can choose to pay for your Rail or Coach travel in the currency of your choice. The VAT that is charged will depend on where you travel and will be shown in the currency of the country in which the VAT will be due.

Why do we tell you the companies in the Trainline group on your confirmation receipt?

The Trainline Group has companies in the United Kingdom (“UK”) and France who facilitate booking your tickets in the UK, the European Union (“EU”) and rest of the world (“ROW”).

When you buy a ticket, whether for travel in the UK, EU, ROW, or a combination, it might be a combination of the Trainline companies facilitating those bookings. The receipts you receive need to show the company that sells you the ticket. Rather than sending you lots of receipts for each ticket from our various companies, we have shown all the ticket details on the one email at the bottom to keep things nice and tidy.

Related Articles

Did you find it helpful? Yes No

Share this post on

Flashback on ECJ Cases – C-220/11 (Star Coaches) – Order – A transport company offering only passenger transport by coach to travel agencies does not fall within the scope of TOMS

On March 1, 2021, the ECJ issued its Order in the case C-220/11 (Star Coaches).

Context: Article 104(3), first subparagraph, of the Rules of Procedure — VAT Directive — Special tax scheme for travel agents — Supply to travel agents of a coach transport service but no other services

Article in the EU VAT Directive

Article 306 1. Member States shall apply a special VAT scheme, in accordance with this Chapter, to transactions carried out by travel agents who deal with customers in their own name and use supplies of goods or services provided by other taxable persons, in the provision of travel facilities. This special scheme shall not apply to travel agents where they act solely as intermediaries and to whom point (c) of the first paragraph of Article 79 applies for the purposes of calculating the taxable amount. 2. For the purposes of this Chapter, tour operators shall be regarded as travel agents.

Article 307 Transactions made, in accordance with the conditions laid down in Article 306, by the travel agent in respect of a journey shall be regarded as a single service supplied by the travel agent to the traveller. The single service shall be taxable in the Member State in which the travel agent has established his business or has a fixed establishment from which the travel agent has carried out the supply of services.

Article 308 The taxable amount and the price exclusive of VAT, within the meaning of point (8) of Article 226, in respect of the single service provided by the travel agent shall be the travel agent’s margin, that is to say, the difference between the total amount, exclusive of VAT, to be paid by the traveller and the actual cost to the travel agent of supplies of goods or services provided by other taxable persons, where those transactions are for the direct benefit of the traveller.

Article 309 If transactions entrusted by the travel agent to other taxable persons are performed by such persons outside the Community, the supply of services carried out by the travel agent shall be treated as an intermediary activity exempted pursuant to Article 153. If the transactions are performed both inside and outside the Community, only that part of the travel agent’s service relating to transactions outside the Community may be exempted.

Article 310 VAT charged to the travel agent by other taxable persons in respect of transactions which are referred to in Article 307 and which are for the direct benefit of the traveller shall not be deductible or refundable in any Member State

- Star Coaches is engaged in the transport of persons by coach in the Czech Republic and between the Member States. It operates that transport either with its own coaches or by using subcontractors, which are transport companies whose transactions are subject to VAT. Its customers are exclusively travel agents established in the Czech Republic or in other Member States. Star Coaches always deals with its customers in its own name. When it has recourse to a subcontractor, it draws up for its customers an invoice mentioning VAT and seeks a refund of the excess tax on the basis of the general scheme of VAT.

- Star Coaches repeatedly deducted large amounts of excess VAT. In this respect the Finanční úřad pro Prahu 5 (Tax Office for Prague 5) considered that the company was supplying travel services and should have applied not the general scheme of VAT but the special scheme for travel agents laid down in Paragraph 89 of the Law on VAT. On 25 June 2008 it issued a VAT recovery notice for January 2008.

- Star Coaches lodged a complaint against the recovery notice. When the complaint was rejected by decision of the Finanční ředitelství pro hlavní město Prahu of 16 December 2008, it brought an action before the Městský soud v Praze (City Court, Prague), which dismissed it by judgment of 18 June 2010. Star Coaches thereupon appealed on a point of law to the Nejvyšší správní soud (Supreme Administrative Court).

- That court entertains doubts as to the application of the special scheme for travel agents laid down in Article 306 of the VAT Directive.

- It notes, first, a difference between the Czech version of that provision and Paragraph 89 of the Law on VAT which transposed the provision into national law. While Article 306 refers to services supplied to travellers, Paragraph 89 covers those supplied to customers of travel agents, an expression which comprehends not only travellers but also other persons. The court points out, however, that there are also differences between the language versions of Article 306 of the VAT Directive and those of Article 26 of Sixth Council Directive 77/388/EEC of 17 May 1977 on the harmonisation of the laws of the Member States relating to turnover taxes — Common system of value added tax: uniform basis of assessment (OJ 1977 L 145, p. 1, ‘the Sixth Directive’), which applied before the entry into force of the VAT Directive, with some versions using the term ‘customer’ and others the term ‘traveller’. It states that actions for failure to fulfil obligations have moreover been brought against several Member States, including the Czech Republic, by the European Commission for using the term ‘customer’ and thus referring, in the Commission’s view, to too broad a class of persons.

- It raises the question, second, should the Court hold that Article 306 of the VAT Directive extends to customers of a travel agent, whether an undertaking such as Star Coaches must be classified as a travel agent within the meaning of that provision. It indicates that, in its view, that is not the case where the undertaking provides only a transport service and no other tourist services. It follows that the present case must be distinguished from Case C‑163/91 Van Ginkel [1992] ECR I‑5723, in which the undertaking concerned, in addition to accommodation, also supplied information, advice and reservation services.

Decision (Order)

A transport company which merely carries out the transport of persons by providing coach transport to travel agents and does not provide any other services such as accommodation, tour guiding or advice does not effect transactions falling within the special scheme for travel agents in Article 306 of Council Directive 2006/112/EC of 28 November 2006 on the common system of value added tax.

Similar ECJ cases

- Roadtrip through ECJ Cases – Focus on ”TOMS” (Travel Operating Margin Scheme)

Newsletters

- BTW jurisprudentie

Advertisements:

VATupdate [email protected]

Support & Info

- Privacy Policy

- Event Calendar

Sign up for our newsletter

I have read and agree to the terms & conditions

Email address:

Leave this field empty if you're human:

Copyright 2021 © - All Rights Reserved - Website development by Supertof Agency

- Our Sponsors

You can search by using one or more of the fields below

Foreign Coach Companies in Germany

Passenger transport is generally liable to VAT in Germany.

The most common case hereby is transport by coach. The transport includes public transport as well as for example, excursions or holiday destination travel. The transport is always subject and liable to tax, regardless whether a domestic or foreign coach company does the transport. If the transport route does not only include Germany, only the route in Germany is liable to tax.

A foreign coach company travelling through Germany is liable to VAT registration in Germany. Furthermore, the form USt1 TU for coaches with a license to travel abroad must be kept in each coach for customs inspection and presented on demand. This form is issued after registration in Germany. If the document is not presented the customs authorities may ask for a security deposit.

Summary of the most important points

- Foreign coach companies travelling through Germany must generally register for VAT with the responsible tax office.

- The most common case is a coach journey through or to Germany.

- The form USt1 TU must be applied for and carried in the vehicle for customs inspection purposes.

Do you have questions?

We can give you the answers. Just send us an E-mail to [email protected] and you will get a respond as soon as possible.

Travel Industry VAT

We have a significant amount of experience in advising a wide range of businesses in the travel sector, including major tour operators, high street travel agents, business travel agents, and online travel businesses. We can help you with a wide range of Travel Industry VAT issues, including:

- VAT efficient structuring (use of purchasing hubs, wholesale structures)

- Implementing transport company arrangements

- Advice on agent versus principal status

- VAT liability of transaction fees and commissions

- VAT refunds on travel agent funded discounts

- TOMS calculations

- In-house supplies

- VAT liability of credit card charges/booking fees

- Exempt revenue streams (eg sale of travel insurance, forex)

CONTACT US BELOW FOR YOUR FREE CONSULTATION:

First Name*

Country of Residence

Your Enquiry*

Communication preferences

Accountancy In Europe Ltd and its subsidiaries will use your email address to provide business news, offers and services we think will be of interest. We will not share your information with any 3rd parties. Read more

Shall We Call You*

—Please choose an option— Yes No

Subscribe to our newsletter*

T ravel industry VAT rules are complex, and the rules differ depending on the capacity in which the business is acting. It is now commonplace for several different revenue streams to be earned from a single customer transaction as businesses seek to replace commission income – this increases the Travel Industry VAT complexity.

The tour operator’s margin scheme (TOMS) is an EU VAT simplification measure originally aimed at traditional tour operators selling package holidays to travellers and preventsthe business from having to register for VAT in numerous EU jurisdictions overseas. The downside however is that VAT has to be accounted for on the entire margin (including the flight proportion) for EU trips; this margin VAT cannot be recovered by customers, even if they in business.

Travel businesses that have historically acted as disclosed agents for VAT purposes and have thus been able to zero rate the fees or commissions they earn on flight sales, can inadvertently fall into the TOMS net if they apply undisclosed mark-ups to their sales of flights. There are a number of Travel Industry VAT mitigation arrangements that can be put in place to prevent the business from having to account for VAT on the sale of flights, but these can often only be put in place prospectively and so do not prevent historic liabilities from arising in this area.

Until January 2010 travel businesses based in the UK were afforded a degree of flexibility in relation to their activities and TOMS, in that they were able to opt out of or into the regime. This was attractive for businesses in the corporate travel sector as they were able to opt out of TOMS and use the normal Travel Industry VAT rules instead, meaning their corporate clients could recover VAT on travel arrangements. The loss of the ‘opt out’ has increased the cost of business travel as TOMS VAT is sticking tax.

Privacy Overview

The General Data Protection Regulation (GDPR) is a regulation in European Union (EU) law on data protection and privacy for all individuals within the EU and comes into effect on 25th May 2018.

GDPR also addresses the export of personal data outside the EU.

As our client, you will now have the following rights:

- The right to correct any incorrect information

- The right to specifically opt-in to any future communications

- The right to have personal data deleted

- The right to stop data being shared

- The right to move data to another organisation

The website www.vatexpertsineurope.com is owned by Accountancy In Europe.com Ltd.

Accountancy In Europe.com Ltd’s Privacy Policy has been updated in line with the new data protection laws in GDPR.

- The information we collect, and process is required for us to be able to perform our contractual obligations and receive payment from you for the accountancy and related services we provide to you.

- We do not sell your personal data.

- We may share your personal data with another party, including a payroll firm in connection with your business and your instructions to us.

- We may share your data where required to be disclosed by law, by any government or other regulatory authority or by a court or other authority of competent jurisdiction provided that and only to the extent it is legally permitted to do so.

- We may also share your personal data with our card payment services provider to enable us to take payment from you by debit or credit card. We keep your personal data only for as long as necessary.

For purposes of GDPR and UK data protection laws, the controller is Accountancy In Europe.com Ltd of The Old Free School, George Street, Watford, Hertfordshire WD18 0BX, United Kingdom.

Our privacy notice is available in full on our website, https://www.vatexpertsineurope.com/data-protection-policy/

Should you have any queries on the above, kindly email us at [email protected]

VAT On Flights: How Much To Pay?

Are you aware of the impact of VAT on flights? While many travelers are familiar with the concept of value-added tax, the specific implications for air travel may not be as clear.

Understanding how VAT applies to flights is crucial for both passengers and airlines alike. It’s not just about the cost of a ticket, but also the complexities of VAT treatment and the potential impact on air travel expenses.

Exploring the nuances of VAT on flights can provide valuable insights into the broader economic and regulatory considerations within the aviation industry.

Overview of VAT on Flights

When considering the value-added tax (VAT) on flights, it’s essential to understand the distinct treatment air travel receives compared to other forms of passenger transport.

Unlike other passenger transport, air travel is subject to specific VAT rates and regulations.

In the UK, certain passenger transport services are zero-rated for VAT, but air travel doesn’t fall into this category. Instead, VAT is charged on air travel at the standard rate.

This means that the cost of flights includes VAT, unlike zero-rated passenger transport services such as some forms of public transport.

The place of supply also plays a crucial role in determining the VAT treatment of flights. For example, flights that depart from the UK are subject to VAT, while international flights may have different VAT implications.

Moreover, the VAT treatment of air travel is further complicated by the imposition of Air Passenger Duty (APD) on flights starting in the UK.

This additional taxation adds another layer to the overall cost of air travel, making it distinct from other forms of passenger transport in terms of VAT and associated charges.

Calculation of VAT on Air Travel

When calculating UK VAT on air travel, you need to consider the different VAT rates for flights, exemptions, and thresholds.

These factors can have a significant impact on ticket prices and the overall cost of air travel.

Understanding how these elements come into play will help you make informed decisions when booking flights and budgeting for your travel expenses.

VAT Rates for Flights

If you’re planning to calculate the VAT on air travel, it’s important to understand the specific VAT rates that apply to different types of flights.

Domestic flights have a unique VAT treatment, as Air Passenger Duty (APD) is imposed on flights starting in the UK, impacting the cost based on the distance and travel class.

Passenger transport in vehicles designed for ten or more people is zero-rated for VAT, whereas private flights in aircraft designed for fewer than ten passengers are subject to the standard rate of 20% VAT.

These VAT rates play a role in reducing traffic congestion and promoting sustainable transport.

It’s essential to consider these rates when accounting for air travel expenses, especially for businesses affected by these VAT exemptions.

Further information on VAT rates for flights can be found on the HMRC website.

Exemptions and Thresholds

To understand the calculation of VAT on air travel, it is essential to be aware of the exemptions and thresholds that apply to different types of flights.

When it comes to air travel, certain passenger transport services are exempt from VAT, while others are zero-rated to the extent that transport takes place.

In the UK, passenger transport in vehicles designed for ten or more people, including aircraft, is zero-rated for VAT.

However, private flights in aircraft designed for fewer than ten passengers are subject to the standard rate of 20% VAT.

The following table summarizes the VAT treatment for different types of passenger transport services:

Understanding these exemptions and thresholds is crucial for accurately calculating the VAT on air travel.

Impact on Ticket Prices

Calculating the impact of VAT on air travel is essential for understanding its effect on ticket prices.

Understanding the different tax treatments for air travel and other expenses is crucial in assessing the overall impact on ticket prices.

Here are some key points to consider:

- Zero-rated VAT for passenger transport in vehicles designed for ten or more people leads to lower ticket prices for scheduled flights, benefiting travelers.

- In contrast, private flights in aircraft designed for fewer than ten passengers are subject to the standard rate of 20% VAT, potentially resulting in higher ticket prices.

- The incorporation of Air Passenger Duty (APD) into ticket prices adds to the overall cost of air travel, impacting ticket prices for passengers.

- Businesses can explore options for recovering VAT on air travel expenses to mitigate the impact on ticket prices.

Understanding these factors is essential for assessing the impact of VAT on air travel ticket prices.

Place of Supply for Passenger Transport

The place of supply for passenger transport, particularly for VAT purposes, plays a crucial role in determining the tax treatment of such services.

For VAT on flights, the place of supply for passenger transport is essential in determining whether the transport element of park-and-ride schemes designed to facilitate the movement of passengers qualifies for the reduced rate.

For instance, passenger transport in vehicles designed for ten or more people is zero-rated for VAT.

However, private flights in aircraft designed for fewer than ten passengers aren’t zero-rated for VAT and are subject to the standard rate of 20% VAT.

Additionally, VAT can’t be claimed back on train tickets or plane fares, making the place of supply a significant factor in the tax treatment of passenger transport services.

Moreover, the recent announcement by the UK Government to cut APD on domestic flights since April 2023 had an impact on the place of supply for passenger transport, especially for domestic flights, further emphasizing its importance in determining the tax implications for such services.

Reduced and Zero-Rated Passenger Transport

When it comes to reduced and zero-rated passenger transport, there are important points to consider.

You’ll want to understand the tax exemptions for flights and how they impact ticket prices.

This topic sheds light on the financial aspects of passenger transport and the implications for both travelers and service providers.

Tax Exemptions for Flights

If you’re traveling in a vehicle designed for ten or more people, your passenger transport is zero-rated for VAT. However, VAT can’t be claimed back on train tickets or plane fares.

When it comes to flights, Air Passenger Duty (APD) is imposed, and private flights in aircraft designed for fewer than ten passengers aren’t zero-rated for VAT.

To qualify for zero-rated passenger transport, the service provider must have a published timetable, and the transport must be provided according to that timetable.

It’s important to note that businesses can utilize Mooncard corporate cards to effectively track expenses related to business travel, including flights and other transportation costs.

Passengers benefit from reduced ticket prices due to the temporary VAT rate cut, intended to stimulate the tourism industry and make air travel more affordable.

However, it’s important to note that train tickets and plane fares aren’t eligible for VAT reclamation.

The reduced VAT rate from 20% to 5% has also temporarily lowered the expenses incurred for transportation that’s subject to VAT, aiming to ease traffic congestion in cities and promote the use of public transport.

Additionally, the UK Government’s announced cut in Air Passenger Duty (APD) on domestic flights since April 2023 had an impact on the cost of air travel within the UK.

While private flights in smaller aircraft remain subject to the standard rate of 20% VAT, the overall aim is to make passenger transport more accessible and affordable.

VAT Liability for Scheduled Flights

Scheduled flights are typically zero-rated for VAT, regardless of the aircraft’s carrying capacity.

This means that the transportation of passengers from one point to another within the UK via scheduled flights isn’t subject to VAT.

However, there are exceptions and additional considerations when it comes to VAT liability for scheduled flights:

- Aircraft Capacity: While scheduled flights are generally zero-rated for VAT, private flights in aircraft designed for fewer than ten passengers are subject to the standard rate of 20% VAT.

- Car Park Services: It’s important to note that ancillary services such as car park facilities provided by airlines at airports are subject to VAT at the standard rate.

- APD Inclusion: Air Passenger Duty (APD), charged by the government to airlines, is incorporated into ticket prices and isn’t directly related to VAT but impacts the overall cost of air travel.

- Business Travel: Businesses can track expenses related to business travel, including VAT liability for flights, using Mooncard corporate cards to ensure compliance with VAT regulations and efficient expense management.

Transport of Disabled Passengers

When considering the VAT liability for scheduled flights, it’s crucial to understand the specific conditions and eligibility criteria for zero-rating VAT on the transport of disabled passengers.

For the transport of disabled passengers, flights are zero-rated if the aircraft is designed or adapted for the carriage of a passenger in a wheelchair or stretcher. This applies both inside and outside the UK.

Furthermore, if the flight is to transport a disabled passenger to or from a destination outside the UK, it may also be zero-rated for VAT.

It’s important to note that these zero-rating provisions apply to the transport of disabled passengers by air, emphasizing the significance of specific regulations for this specialized service.

Understanding these VAT regulations and exemptions is crucial for businesses and individuals involved in the transport of disabled passengers, ensuring compliance with the necessary conditions for zero-rating VAT on flights designed or adapted for the transport of disabled passengers.

Ancillary Services to Passenger Transport

Ancillary services to passenger transport, such as restaurant meals, theatre trips, and limousine transport to or from an airport, provide additional convenience and comfort to travelers.

These services enhance the overall travel experience and cater to the cultural interests of passengers.

When it comes to zero-rated domestic passenger transport, activities like pleasure cruises, cliff lifts, and excursions by coach or train fall under this category.

It’s important to note that certain arrangements for a supply of zero-rated passenger transport can also be zero-rated when made by an agent.

Additionally, businesses may be impacted by the exemption of private flights in aircraft designed for fewer than ten passengers from zero-rated VAT on flights.

This exemption affects the overall cost of passenger transport and ancillary services, which could influence the choices and preferences of travelers.

Therefore, understanding the nuances of zero-rated options in passenger transport and ancillary services is crucial for businesses and travelers alike.

VAT on Cruises and Ferries

If you’re planning a cruise or ferry trip, it’s essential to understand the VAT implications that may apply to your journey.

Cruises and ferries are generally subject to standard VAT rates.

However, depending on the specific circumstances, some passenger transport services on ferries and cruises may qualify for reduced VAT rates or be zero-rated.

The VAT treatment is influenced by factors such as the type of service provided and the destination of the journey.

It’s important to consider the nature of the transportation that’s being provided and any ancillary services offered to fully understand the VAT implications.

Complex considerations, such as schemes designed to reduce VAT for certain passenger transport services, may come into play.

Seeking professional advice can be beneficial, as VAT regulations for cruises and ferries can be intricate.

According to a published source, the VAT treatment of cruises and ferries depends on factors such as the type of service, the destination of the journey, and any ancillary services provided.

Therefore, it’s advisable to carefully assess the VAT implications when planning a cruise or ferry trip.

Frequently Asked Questions

What is vat on airline tickets.

VAT on airline tickets is a tax levied on the transaction value of the ticket.

In the UK, the government temporarily reduced the VAT rate on airline tickets from 20% to 5% to boost the tourism industry.

What Is VAT on Travel?

When you travel, VAT may apply to expenses like accommodation, food, and souvenirs. It’s currently reduced to 5% in the UK for the tourism industry to support businesses.

Keep this in mind when planning your next trip.

What Is VAT in Aviation?

VAT in aviation refers to the value-added tax applied to air travel and related services. It falls under a different treatment compared to other transportation expenses, with certain exemptions and regulations.

Is VAT Charged on Local Flights?

Yes, VAT is not charged on local flights, as they fall under zero-rated passenger transport services. This applies to flights with at least 10 seats, including those for the pilot and crew.

So there you have it, VAT on flights is a complex and confusing topic that will leave you scratching your head for days.

With all the different rules and regulations, it’s a wonder anyone can figure out how much tax they’re actually paying.

But hey, at least now you know a little bit more about the wild world of air travel taxes.

Good luck out there!

- Recent Posts

- Ireland Vat Calculator Dublin – Standard Rate in Irish is 23% - February 28, 2024

- Income Tax or VAT: Which Tax System is Better for the Philippines? - February 4, 2024

- Union and Non-Union OSS for VAT Compliance in Europe: What’s the Difference? - February 4, 2024

Similar Posts

Australian vat with updated vat rates & exemptions.

The standard VAT Rate is 10%. Now you can calculate the vat bill with our Vat Calculator Australia. Australian Vat…

Vat Calculator India – Standard tax Rate in India is 18%

The Standard VAT Rate in India is 18%. Now you can calculate the tax with our Vat Calculator India. Goods…

What Are the VAT Compliance Services Provided by Tax Professionals in Ireland?

Ah, the joyous world of Value-Added Tax (VAT) compliance in Ireland, where the only thing certain is that you’ll need…

How to transfer money from India to USA without tax

How to transfer money from India to USA without tax? you may be concerned about the taxes and fees involved…

Taxes and Moving Companies in Johannesburg: What You Need to Know

In South Africa, moving companies, especially in Johannesburg, play a vital role in helping people transition to new spaces. But,…

Morrisons VAT Receipt – Everything You Need To Know!

When it comes to managing your expenses, keeping track of your VAT receipts is crucial. But have you ever wondered…

Jon Jenkins

Is There VAT on Train Tickets? (Zero Rated or Exempt)