Travel and Expense

How to do an expense report: steps and solutions for effective expense reporting.

There's nothing like face-to-face communication, but travel can be one of the biggest costs associated with doing business. Detailed and accurate expense reports help you keep your finger on where money is going, while employees get reimbursed for expenses promptly.

Travel-related expenses at small and medium businesses increased 178% in 2022. Everyone who travels for your business should know how to do expense reports. Employees who pay out of pocket want to have their expenses reimbursed. When tax time comes, you need to be able to accurately document legitimate business expenses. And, the business intelligence associated with travel costs means understanding your expenses better.

Setting up a consistent system means that you’re always on top of all costs and using your travel funds effectively.

Why a Well-Structured Expense Report Matters

A business expense report has to be set up in a way that’s easy to understand, comprehensive, and consistent across departments and personnel.

A good report gives the business a better idea where travel-related money is going and can help with planning. For example, you can see whether you need to budget more toward international airfare in the coming year or decide whether travel-related subscriptions are paying for themselves and being used to their fullest potential. You can also identify places where you can save money.

Business travel expenses are typically tax-deductible. With the right expense report setup, you can document those expenses quickly and easily, saving headaches at tax time.

A Step-by-Step Guide to Expense Reporting

An expense report is a document that brings together all the relevant expenses from a business trip or event. This will include information like the date of a purchase, the amount spent, the expense category, and any relevant receipts.

Start by collecting receipts during travel. Physical receipts should be either scanned or photographed so the information is available to anyone who needs it later on for documentation.

Capture all the relevant information in the business expense template or system used. This will include:

- Date of the expense

- Vendor purchased from

- Expense category (common categories include meals, transportation, and lodging)

- any tax or VAT assessed)

- Any additional notes

- A PDF, PNG, or JPEG of the receipt of invoice

This data is sent to the person in charge of managing expenses. Then, expenses that need to be reimbursed are tallied up and paid. When it's time to make reports for tax and other purposes, all the data is there and available in one place.

How Templates Can Help

If everyone's working with the same framework, expense reports get a lot easier for everyone involved. Your traveling employees have a better handle on what expenses are reimbursable. You are better able to categorize expenses, so you can see where your money is going.

Exploring Tools for Expense Reports

There are a few different tools you can use to do your expense reports. Each has their own benefits and drawbacks.

At the most informal end, you can simply have traveling employees email a list of expenses and attach images of receipts. However, this can be a hard system to standardize and it creates opportunities for risk. You'll likely end up with people formatting their reports differently from one another, such as using different wording for the same expenses. It can be easy to miss legitimate expenses. Plus, parsing the list can use huge amounts of your finance team's time that could be better spent on other tasks.

You can learn how to do an expense report in Excel, but this has limitations. Using an incorrect formula in one cell can populate an error throughout your sheet. And, the spreadsheet is what's known as a "closed" system. You can't automatically export data from it into another system.

Specialized, purpose-built tools like the ones from SAP Concur can cut the confusion and make travel expense reporting easy and accurate. Traveling employees can start by collecting receipts in the ExpenseIt mobile app. Then they upload images to Concur Expense , which creates and categorizes expenses automatically. If you are using Concur Drive , it will seamlessly capture mileage to ensure expenses are documented accurately and fairly.

Common Challenges in Expense Reports

While expense reports are necessary for transparent operation of your business, they can also be challenging for both traveling employees and the people coordinating back in the office.

Fraud is, unfortunately, a persistent risk associated with business travel. Studies show that around 5% of a typical organization's annual revenue is lost to fraud. Employees may deliberately or unintentionally request reimbursement for expenses that are not legitimate parts of business travel. A well-organized system with clear categories can help eliminate misunderstandings and ensure reimbursement requests are accurate.

Many employees do not want to spend the time associated with paperwork after business trips. A system like SAP Concur solutions, however, captures and categorizes most expenses automatically . All the employee needs to do is review the inputs to ensure accuracy and it's good to go.

Speed and Simplify Your Expense Report Process

Travel expense reports provide essential insights into where your travel-related funds are being spent. They provide the business intelligence you need to keep your travel cost-effective and to get the most out of every travel dollar spent.

Want a one-stop solution that makes everything easier? Our self-guided demo shows you how to capture expenses from any device, submit an expense report to a manager, and see how to approve reports you receive.

How to calculate Germany’s per diem rates in 2023 / 2024

Published on November 28, 2023

"travel expense report deutsch")

Germany is known worldwide for its cultural commitment to efficiency and attention to detail. For the most part, these ideas have served the nation well - it boasts the fourth-largest economy in the world; first in Europe.

But in some cases, efficiency and precision butt heads against one another. And business trips are one of those cases.

Employees in German companies have fixed per diem rates to cover travel expenses . These are set by the government, which in theory makes things more efficient. Companies don’t need to create their own policies - they just follow the rules.

But there’s a problem: the rules are fairly complex, and lots of businesses struggle to follow them.

Efficiency, meet precision.

In this article, we’re going to give you a clear overview of the law for business travel within Germany and abroad.

Please note: This article contains per diem rates and rules for 2024 (in place since 2021). You can find applicable flat rates for the most common destinations further down in this article.

What are per diem rates?

This will probably be clear to most readers, but it’s important that we set out just what we’re talking about. While travelling for work, certain costs are incurred by the employee and should be reimbursed by the company .

Some costs are expected to be covered your per diem, and therefore don’t need to be claimed separately. You’ll simply want to keep these costs below the daily per diem rate you’ve been allocated.

Other costs aren’t covered by your per diem, which means you should include them in an expense claim .

Covered by per diem

These will fall under the fixed rates below, and should not be claimed separately .

Meals purchased while travelling for work

The law (see below) only talks about meals. Some employees will choose to include other small costs (metro tickets or stationery for example), rather than seeking reimbursement for these minor items.

Not covered by per diem

These expenses should still be reimbursed by the company as part of a separate expense claim .

Transport to and from the airport or meetings

Accommodation if staying overnight

Meals and other costs incurred while meeting clients

Keep this distinction in mind when travelling. Now, let’s look at the specific rules for per diems.

The law around German per diem rates

The applicable law in this case is the statute on income tax - more precisely section 9, paragraph 4(a) (link in German). This covers meals for travelling workers, and essentially states the following:

If the employee works outside their home and first place of work (external occupational activity), a lump sum for meals is paid in compensation for the additional expenses.

[The actual rates paid are in the next section of this post.]

Since it would be time-consuming, complicated, and potentially unfair to have individual businesses set their own rates, the government does it for them. So as long as the rates are easy to understand and make sense, this is a good thing.

It also prevents the need for itemized expense claims - something employees generally hate . You don’t need to submit every receipt and take hours filling in expense reports. If you travel for X number of days, you receive Y in reimbursement.

The rates depend on travel duration and destination (see table below).

Note : You can’t claim these rates twice.

Two fee rates for all business trips

At the end of each year, the Federal Ministry of Finance publishes the applicable meal allowances for the following year. For the first time in many years, the flat rate allowances for business travel were updated in 2020.

Although the lump sums have changed for some countries, the basic principle remains the same. Since January 1, 2014, only two meal per diems apply, both within Germany and abroad. These are based on the travel duration:

Small meal allowance : for business trips lasting more than eight hours and less than 24 hours. This rate also applies to arrival and departure days of multi-day business trips.

Large meal allowance : For business trips that last longer than 24 hours. This rate is applied to every single day.

Important note : The expense calculation is based on full calendar days . In fact, to claim a full day, the traveller actually has to be away from home (or the office) from 0:00 to 24:00.

Anyone who went on a business trip before 2014 will find that a few things have changed with the reform of travel expenses. The most important change: business trips with a duration of less than eight hours can no longer be billed .

Current per diem rates in Germany

The rates for business travel in Germany changed slightly in 2020, for the first time in years.

Even with the 2014 reform, only the categories were changed, but not the amount of the lump sums. So this 2020 update is worth noting.

Today, these are the lump sum amounts for German per diems :

For business trips with a duration of less than 24 but more than eight hours, €14 can be noted in the travel expense report.

With a minimum duration of 24 hours, €28 euros can be claimed for each full day, and €14 euros for arrival and departure days (which will obviously be less than 24 hours).

The overnight flat rate is €20 - to be used for accommodation. In reality, accommodation will usually be covered fully by the employer , so travelling employees won’t claim this cost. But in cases where accommodation is not covered - for freelancers, for instance - this cost can usually be claimed through an individual’s income taxes.

Why is the overnight lump sum so low? One theory is that this should prevent fraudulent charges if business travellers choose to stay with friends or relatives.

You can find an example calculation in our free travel expense report template .

Exceptions to these rules

No good rules or regulations would be complete without exceptions. Thankfully, in this case they’re simple and quite brief.

First, the food allowance will only be paid in full if the business traveller actually pays for their own food . If the employer pays for meals on the trip, the rate will be reduced accordingly:

If breakfast is included (in the hotel fee, for example), 20 percent of the flat rate will be deducted for the day.

If lunch or dinner is provided by the employer, 40 percent of the fee will be removed.

For shorter business trips, it should be noted that meals provided by the employer are subject to income tax. Here are the so-called non-monetary benefits which must be taken into account in at tax time :

For breakfast, the value is currently €2.00.

For a lunch or dinner, €3.80 will be charged.

Foreign packages for business travel

As already mentioned, the categories for food allowances for business trips in Germany and abroad apply equally. But the rates of reimbursement may differ significantly depending on the country .

While an overnight stay in London, for example, costs €163, in Rome the value is only €150. For a day in Tokyo, the package is €50, but in Athens it's only €40.

The list also includes prices in different regions in the same country. For example, a stay in Miami is more expensive than in Los Angeles.

Unlike the lump sums for business travel within Germany, the rates for foreign destinations are frequently adjusted .

To help, we put together a list with the most frequented destinations and their respective meal allowances in this article. (at the bottom).

You can find the complete list here .

German per diems: clear as mud

Hopefully this article has helped to clear up some of the confusion around the German per diem system. In some ways it all seems unnecessarily complex, but once you have the basic concepts it should be fairly simple to repeat regularly.

The key parts to remember are the specific rates you can claim for each day, and that you can’t claim costs that have already been covered by your employer .

To help you manage your next business trip and keep on top of all spending (per diem or not), download our free Expense Report Template below.

More travel articles

VAT and expenses for UK businesses

10 excellent business travel management tools for 2023

The complete guide to corporate travel management

More reads on Business travel spend

"travel expense report deutsch")

UK per diem: how HMRC meal allowance rates work

"travel expense report deutsch")

How modern CFOs easily optimize travel spending

Get started with spendesk.

Close the books 4x faster , collect over 95% of receipts on time , and get 100% visibility over company spending.

- NETHERLANDS

- SWITZERLAND

Expat Info Articles

How to claim travel expenses on your German tax return

The reason so many people choose to submit a tax return in Germany, even if they are not obliged to, is so that they can reduce their tax bill by taking advantage of deductions. One of the easiest deductions you can make is for your travel expenses to and from work. wundertax explains how it’s done.

Travel expenses for professional-related commutes can be claimed by taking advantage of the commuter allowance ( Entfernungspauschale ) on your German tax return and help increase your chances of a tax refund.

While some expenses are deducted as a set sum (e.g. per kilometre travelled), others can be deducted in full (e.g. the cost of tickets). Traditional employees can deduct these costs as income-related expenses ( Werbungskosten ) while freelancers / self-employed people can claim their travel expenses as business expenses ( Betriebsausgaben ). In this article we will be focusing on:

- Expenses for the commute from your residence to your primary workplace

- Travel costs for external activities and business trips

1. Deducting expenses for your work commute

You can claim a commuter allowance for commutes between your residence and primary workplace ( erste Tätigkeitsstätte ). This allowance amounts to 30 cents per kilometre for the first 20 kilometres of one-way travel to or from your workplace, regardless of means of transportation or actual incurred expenses.

That means this can be claimed whether you walk, ride a bike, drive a car, ride as a passenger, or take public transportation. The tax office will only accept deductions for the shortest possible route.

As of January 2021, the commuter allowance was increased to 35 cents from the 21st kilometre of one-way travel for long-distance commuters and from 2022 to 2026 it will be increased again to 38 cents from the 21st kilometre of one-way travel.

Is there a limit to the commuter allowance?

Generally, the tax office accepts 230 trips per year, but if you have a six-day work week you can claim up to 280 trips per year. Commuter expenses cannot be deducted for days spent home sick, on vacation, or working from home – days spent working from home can instead be claimed using the Home Office Lump Sum.

A maximum of 4.500 euros per year can be deducted with the commuter allowance. However, if you meet one of the following two exceptions, you should hang on to receipts as proof for the tax office:

- If you commute to work in your own personal or business vehicle you can claim more than 4.500 euros per year.

- If you commute to work by public transportation and the costs exceed 4.500 euros per year, you can enter and claim the actual expenses on your tax return.

Commuter costs for multiple workplaces

You can only have one primary workplace per employment role. If you work at several locations, this is considered external activity ( Auswärtstätigkeit ) and treated differently.

Rather than claiming a lump sum per kilometre, if you commute to external activities by public transport, you can have your actual expenses reimbursed (e.g. the cost of your tickets). If you travel by car, you can take advantage of the kilometre allowance ( Kilometerpauschale ). This applies to both the outward and return journey and amounts to 30 cents per kilometre.

If you have several different jobs in different locations, however, you can claim the commuter allowance for each primary workplace, so long as you travel home in between. When travelling from primary workplace to primary workplace, the distances can be added together, but then the commuter allowance can only be used for half of the total distance.

Mobility premium for long-distance commuters

As of 2021, long-distance commuters with a daily commute of 21 kilometres or more can apply for the new mobility premium ( Mobilitätsprämie ), which grants a bonus of 14 percent of the increased commuter allowance from the 21st kilometre of one-way travel.

To apply for this premium, your annual income cannot exceed the basic tax-free allowance ( Grundfreibetrag ), which amounts to 9.744 euros as of 2021. As of 2022, the basic tax-free allowance increased to 10.347 euros.

You can apply for the mobility premium in your tax return, and if you meet the requirements, it is transferred directly to your bank account. The assessment basis for the premium varies depending upon the difference between your annual taxable income and the basic tax-free allowance.

2. Costs for business trips

If you travel for work for any purpose including field services, further education, and trade fair visits, it’s recommended to claim the resulting expenses on your tax return (provided your employer didn’t already cover them). Your means of transport are irrelevant unless you’ve travelled in a company car, which is not tax-deductible.

Expenses for travel by public transport, ship, or aeroplane are all reimbursed in full so long as you travelled in the lowest class available. Train journeys in the next class up can be reimbursed if the travel time exceeds two hours.

If you travelled by car, you can either determine the actual incurred costs and claim them or use the kilometre allowance ( Kilometerpauschale ). Unlike the commuter allowance, the kilometre allowance can be applied to both the outward and return journeys.

Per kilometre travelled, the kilometre allowance amounts to:

- 30 cents for trips by car

- 20 cents for trips by motorcycle, scooter, moped, or e-bike

If your employer covered a portion of your business trip expenses, you have two options: You can either deduct the amount from the total expenses or you can write off the employer subsidies on your tax return.

If your business trip away from home and your primary workplace exceeds 8 hours, you can claim a flat rate of 14 euros for meals ( Verpflegungsmehraufwand ). If the trip exceeds 24 hours, you can claim a flat rate of 28 euros.

The rules surrounding commuter costs and other travel expenses can be complicated. wundertax helps you complete your tax return in as little as 17 minutes, while giving tips on deductible costs, so you can maximise your refund. Get started now .

Natascha Manthe

Natascha works as a Content Manager at wundertax. She loves to dive into tax topics and put them into easy-to-understand form. The other half of her heart belongs to acting:...

JOIN THE CONVERSATION (0)

Leave a comment

- How it works

- Try it out for free

- Expenses from Your Profession

Claim Travel Expenses on Your Tax Return

Travel expenses for professional-related commutes can be claimed as income-related expenses (Werbungskosten) on your tax return and help increase your chances of a tax refund. These expenses can include business trips, trips home in the case of double household management, or simply your daily commute to work – To learn more about deducting these on your tax return, keep reading this article!

Which travel expenses can be claimed?

Travel expenses incurred for professional reasons can be claimed on your tax return by entering the appropriate lump sums or flat rate and in some cases, these costs are fully deductible. These can be divided into 3 categories:

- Expenses for the commute from your residence to your primary workplace

- Travel costs from your secondary to primary residence in the case of double household management

- Travel costs for external activities & business trips

Traditional employees can deduct all of these costs as income-related expenses while freelancers/self-employed persons can claim their travel expenses as business expenses (Betriebsausgaben).

1. Your work commute

Primary profession: commuter allowance.

You can claim a commuter allowance (Entfernungs-/Pendlerpauschale) for the commutes between your residence and your primary profession . Primary profession refers to your main and permanent job. Freelancers can claim the commuter allowance for commutes to their first business location while students/trainees can claim it for commutes to their place of education.

The commuter allowance amounts to 30 cents per kilometer for the first 20 kilometers of one-way travel to or from your workplace, regardless of means of transportation or actual incurred expenses. That means this can be claimed whether you walk, ride a bike, drive a car, ride passenger, or take public transportation – just keep in mind that you can only claim one-way per working day. The tax office will only accept deductions for the shortest possible route (regardless of means of transport) and long detours would have to be justified, for example, if it’s more convenient and is a faster route (due to the shorter route having heavy traffic etc.).

Note: As of January 2021, the commuter allowance was increased to 35 cents from the 21st kilometer of one-way travel for long-distance commuters and from 2022 to 2026 it is increased again to 38 cents from the 21st kilometer of one-way travel.

Commuter allowance: Maximum limit

Generally, the tax office accepts a flat rate of 230 trips per year for a 5-day work week, and 280 trips for a 6-day work week. Commuter expenses can not be deducted for days spent home sick, on vacation, or working from home – days spent working from home can instead be claimed using the home office lump sum . A maximum of 4,500 euros per year can be deducted, unless you meet one of the following two exceptions :

- If you commute to work in your own personal or business vehicle and exceed 4,500 euros per year with the commuter allowance, the excess amount may be deducted.

- If you commute to work with public transportation and the costs exceed 4,500 euros per year, you can enter and claim the actual expenses on your tax return (not as a part of the commuter allowance).

If you meet either of these exceptions, hang on to your receipts as proof must be submitted upon the tax office’s request.

Commuter costs for multiple workplaces or professions

There can only be one primary workplace per profession, if you work at several locations they are considered external activity (Auswärtstätigkeit). Expenses for commuting to external activities can be reimbursed if you travel by public transport and the kilometer allowance (Kilometerpauschale) can be used if you travel by car. This applies to both the outward and return journey and amounts to 30 cents per kilometer.

If you have several professions , the commuter allowance can only be used for your primary profession if you travel between there and home on the same day. If you travel from workplace to workplace, the distances can be added, but then the commuter allowance can only be used for half of the total distance .

Mobility premium for long-distance commuters

As of 2021, long-distance commuters with a daily commute of 21 kilometers or more can apply for the new mobility premium (Mobilitätsprämie). In order to apply, your taxable income must not exceed the basic tax-free allowance (Grundfreibetrag) of 9,744 euros (as of 2021). The bonus is based on the 2021 commuter allowance increase and will remain valid until 2026. If eligible, you can apply for this premium directly on your tax return and receive it directly to your bank account. The premium grants a bonus of 14% to the already increased commuter allowance from the 21st kilometer of one-way travel to work and the assessment basis for the premium varies upon the difference between your annual taxable income and the basic tax-free allowance.

2. Commutes to your main residence with two households

Many employees manage two households for professional purposes and shorter commutes to the office, leading to common trips between their primary and secondary residences. One trip per week (or a total of 46 per calendar year) back to your primary residence can be deducted using the commuter allowance regardless of means of transportation. The same rules apply: either the outward or return journey can be deducted. The allowance can be deducted even if no costs were incurred from the trip, such as if you were given a ride.

In order to be eligible to deduct costs for double household management , your “life core” must take place at your primary residence, where you regularly stay and contribute at least 10% of the costs. It is not a prerequisite to have a spouse, partner, or child(ren) living at your primary residence.

The commuter allowance increase to 35 cents (2021) / 38 cents (2022) from the 21st kilometer also applies to trips home to your primary residence to see your family. Note: The maximum of 4,500 euros per year doesn’t apply to family trips home.

If you travel with public transportation and the costs exceed the benefits from the commuter allowance, you can instead deduct those costs individually on your tax return. If you fly home, you can only claim the price of the plane ticket.

Note: Weekly trips to your primary residence cannot be deducted if made with a company car. No tax must be paid on the first trip home with a company car as a non-cash benefit (geldwerter Vorteil), but it must be taxed from the second trip onwards.

3. Costs for business trips

Employers often pay for business trip expenses out of their own pocket – whether it be field service, further education, or visits to a trade fair. If the costs aren’t covered by your employer, it’s definitely worthwhile to claim them on your tax return. Means of transport are irrelevant unless you’ve traveled in a company car , which is not tax-deductible.

Expenses for travel by public transport, ship, or airplane are all reimbursed based on the lowest class available. Train journeys exceeding two hours in the next higher class can be reimbursed.

If you traveled by car, you can either determine the actual incurred costs and claim them or use the kilometer allowance (Kilometerpauschale). Unlike the commuter allowance, the kilometer allowance can be applied to both the outward and return journey .

Per kilometer traveled, the kilometer allowance amounts to:

- 30 cents for trips by car

- 20 cents for trips by motorcycle, scooter, moped, or e-bike

Tip: If your business trip away from home and your workplace exceeds 8 hours, you can claim a flat rate of 14 euros for room and board as well as meals (Verpflegungsmehraufwand). If the trip exceeds 24 hours, you can claim a flat rate of 28 euros.

Please note: The portion of travel expenses covered by your employer can no longer be included in your tax return. You can alternatively declare the costs in full if you also claim the employer subsidies for your travel costs.

Is it worth it for you to file a tax return?

Related articles.

- Tax Forms for your 2021 Tax Return

- What exactly is double household maintenance?

- How to Deduct Bahncard from Tax with Travel Expenses

- Call us: +43 664 414 8087

- Email: [email protected]

German travel expenses in Dynamics 365 / Deutsche Reisekostenabrechnung 2022

- Eugen Glasow

- January 4, 2022

Travel expense reporting in Germany may be implemented in Dynamics 365 for Finance with literally no customizations. A special attention must be paid to the per diem calculation.

Introduction

In general, per diem in Germany is an allowance for catering. Hotel bills are reimbursed in full. An employee of a German company – let’s call her Erika Mustermann – typically gets reimbursed for meals a fixed statutory amount per day. If she is paid above the legally prescribed daily rate, the difference would be subject to her income tax.

For domestic trips within Germany she becomes 28 Euro per day, yet this full rate is only applied from the second day on multi-day business trips. For the first and the last day Erika becomes only ½ of the daily ration = €14:

Erika is obliged to report every free meal sponsored by the employer or customer, reduce the daily allowance in accordance with the “20-40-40” rule:

The statutory per diem rates vary by country and sometimes specific to a city. The rates are regularly updated by the federal government and rounded to full euros: https://factorialhr.de/blog/verpflegungspauschale-2022/ . The “20-40-40” meal reduction rule also applies to destinations abroad, based on the full 24h rate.

In the following chapters 4 distinct realistic cases are explored, with the appropriate setup in Dynamics 365 for Finance:

Domestic business travel – Case 1 “One-day training”

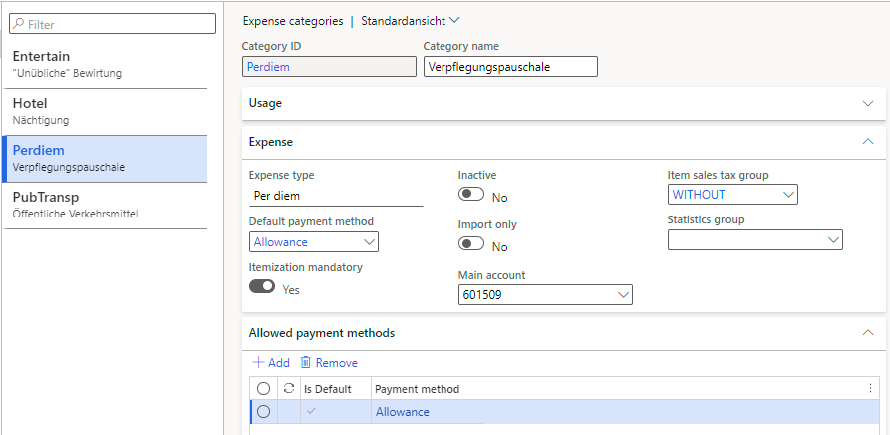

The Calculate meal reduction by may be set to either Meal type per day and Meal type per trip , since the breakfast weights less than lunch/dinner and the meal reduction amount stays the same for the first/last/middle day.

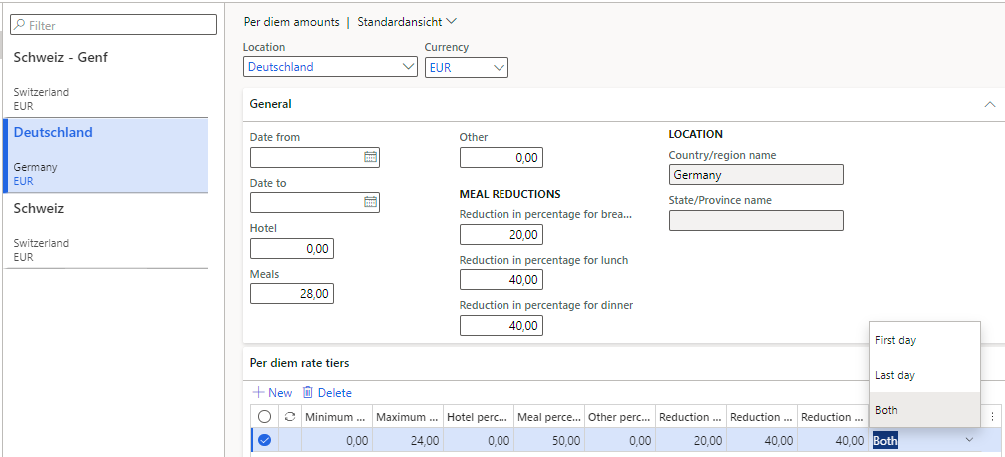

Per diems locations shall be created next. Every leg in on the business trip has to be given a “location” to deduct the right allowance for that country or city. The rate per location is assigned here: Expense management> Setup > Calculations and codes > Per diems . The fist and the last day assume a reduced allowance, this can be modelled by means of the Per diem rate tiers :

The reduction (€14/€28 = 50%) is the same for the day of arrival and the day of departure, therefore the most concise setting is Apply to = Both . On an overnight stay, the 8 hours threshold is ignored: in the above examples 2-4 the first day is eligible despite it only lasted 24:00-18:00 = 6 hours. Therefore we may not set Minimum hours = 8; the threshold can be enforced differently with a customized “Expense report policy”, see below.

We now can test Case 1, but first make sure that the Meal reduction, Breakfast, Lunch, Dinner, Location fields are activated in the Expense management > Setup > General > Display fields .

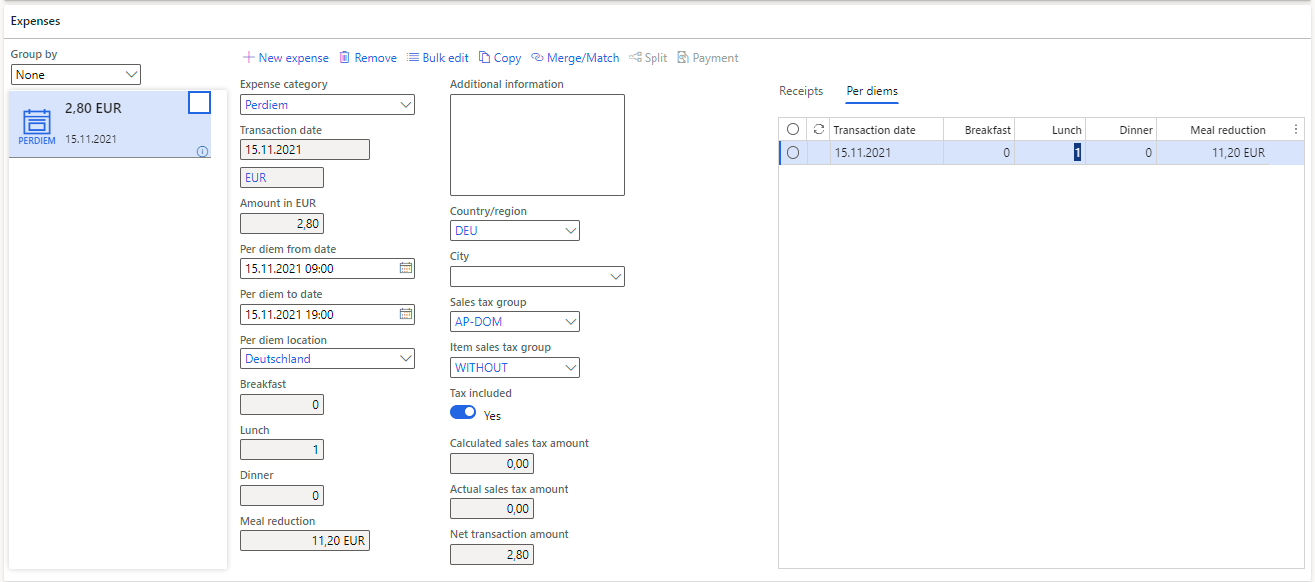

In Expense management > My expenses > Expense reports , add a new report, choose the location, add a new line PerDiem . The UI automatically switches to the detailed mode where you can enter the start and the end date/time of your trip and choose the Per diem location:

On the Per diems tab, set Lunch = 1 . The reduction of €11,20 is applied as expected, and the total allowance amount becomes €2,80. To post the expense report an approval workflow has to be in place.

Remember, a one-day trip less than 8 hours does not count as business travel. The per diem rate tiers cannot be used to enforce it, but here are 2 possible alternatives:

- solve it organizationally, establish “human-driven” approval rules

- make a small extension to the class TrvRuleExpressionSetup to enable the total trip duration, the start and the end date as parameters in the expense policy definition:

public FromDate parmPerDiemFromDate(CompanyId _companyId, TableId _tableId, RecId _recId) { TrvExpTrans trvExpTrans = TrvExpTrans::find(_recId); return DateTimeUtil::date(DateTimeUtil::applyTimeZoneOffset(trvExpTrans.DateFrom, DateTimeUtil::getUserPreferredTimeZone())); } public ToDate parmPerDiemToDate(CompanyId _companyId, TableId _tableId, RecId _recId) { TrvExpTrans trvExpTrans = TrvExpTrans::find(_recId); return DateTimeUtil::date(DateTimeUtil::applyTimeZoneOffset(trvExpTrans.DateTo, DateTimeUtil::getUserPreferredTimeZone())); } public Hours parmPerDiemHours(CompanyId _companyId, TableId _tableId, RecId _recId) { TrvExpTrans trvExpTrans = TrvExpTrans::find(_recId); return any2real(DateTimeUtil::getDifference(trvExpTrans.DateTo, trvExpTrans.DateFrom)/3600); }

Continued…

Here: German travel expenses in Dynamics 365 – Part 2

Expense management blog series

Further reading:

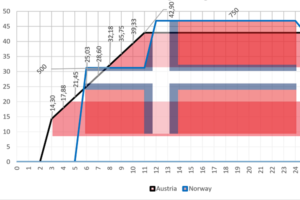

German travel expenses in Dynamics 365 Part 2 German travel expenses in Dynamics 365 / Deutsche Reisekostenabrechnung 2022 On currency in credit card expense transactions Part 2 On currency in credit card expense transactions Part 1 D365: Import Mastercard CDF3 statements OOTB Configuring Austrian and Norwegian per diems in Dynamics 365

Hi Eugen, many thanks for this blogpost. I have a question regarding “Case 1”. My customer is saying that for the departure day, the meal deduction should be relative to the reduced daily allowance rate; so for instance lunch reduction should be 40% of 14 EUR and not 40% of 28 EUR. Do you know if this is supported? Thank you, Fjorela

Just update these to 10%-20%-20% Can they prove it? A law, URL link, a court or a ministerial edict? Because this does not make a lot of sense: if you’ve eaten a lunch the 1st day, will you use just a half of its nutritional energy sitting in the train on the day of arrival? 🙂 I know, the laws are often nonsensical.

Leave A Reply Cancel reply

Save my name, email, and website in this browser for the next time I comment.

Reimbursement of travel expenses – general information

Reimbursable travel expenses.

You may be reimbursed for costs incurred during official travel in accordance with Section 77 of the State Civil Service Act (Landesbeamtengesetz) in conjunction with Section 1 (2) of the German Travel Expenses Act (Bundesreisekostengesetz - BRKG).

Compensation for travel expenses includes:

- Reimbursement for transport (Section 4 BRKG)

- Compensation for distance travelled (Section 5 BRKG)

- Per diems (Section 6 BRKG)

- Accommodation expenses (Section 7 BRKG)

- Reimbursement of expenses during extended stays (Section 8 BRKG)

- Expense and flat rate compensation (Section 9 BRKG)

- Reimbursement of other costs/other incidental expenses (Section 10 BRKG)

All other travel expenses not listed here are considered general living expenses and cannot be reimbursed.

Detailed information about reimbursement can be found on the linked pages.

Advance payment

Official travel often involves expenses necessary to conduct official business. However, these expenses can generally only be settled or reimbursed after the approved official travel is completed and you submit a travel expense report.

To avoid paying the total amount in advance, you can apply for advance payment of official travel with expected costs of more than 200 euros. Advance payment is made for 80% of the expected expenses and must be requested using the official travel request form. Include your personnel number and send the request form to the Travel Expense Office.

This partial payment is then offset against the travel reimbursement to be paid after completion of official travel. If your partial payment is greater than your actual travel expenses, you are required to return the overpayment.

If you plan to extend official travel with a private stay, please read our detailed information about this option, particularly regarding a cost comparison of departure and arrival costs. You must submit the cost comparison when requesting advance payment.

Reimbursement

Advance payment is not the same as travel expense reimbursement. You must request reimbursement of travel expenses following the end of official travel, no later than 6 months after the trip . Please submit your request electronically or in writing to the Travel Expense Office.

Please submit the completed travel expense report together with the following original documents:

- Approval of the official travel

- Transport tickets and receipts (e.g. public transit tickets)

- Airline tickets and receipts

- Receipts for incidental expenses

- Hotel invoices

- Invoices for participation fees, seminar or workshop fees

If you only have a print-out of a digital receipt or invoice, please write "Online-Beleg! - gilt als Original" on this together with your signature, name, and the current date. This is required pursuant to the circular " Vordrucke u. ergänzende Haushaltswirtschaftliche Regelungen " (only in German) of 10 February 2017.

Application

- Application for conducting travel by non-TU personnel (pdf, 115 KB)

- Application for official travel (pdf, 128 KB)

- Attachement - Reimbursement for Travel Expenses (pdf, 159 KB)

- Attachment for Reimbursement Claim (pdf, 159 KB)

- Traveling expenses for interviews (docx, 39 KB)

- German Travel Expenses Act (BRKG)

- General BRKG Administrative Provisions

Contact & Location

Sandra Hoffmann

+49 30 314-22988

+49 30 314-24601

Torsten Radmann

- Login Declaree

- Business Credit Cards

- Expense Automation

- Expense Compliance

- Data & Insights

- CO2 Reporting

- Marketplace

- Integrations

- Case Studies

- Release Notes

Germany's 3-Month Rule And How to Ensure Compliant Expenses

Updated in January 2023

A critical issue (or the sudden outbreak of a pandemic) may lead business travellers to spend more time away from home than initially planned.

Because such trips are work related, employers are responsible for covering the traveller’s daily meals. They can do this either with regular receipt-base reimbursements, or by paying the traveller an allowance. In the latter case, it is important to note that allowances cannot be paid tax-free indefinitely and are limited to a three-month period.

Below we review the 3-month rule, exceptions, and how to manage expense report compliance with this specificity of the German market .

What is the German "3-month rule"?

Per diems (daily allowances) for daily expenses are only tax-free for up to three months of continuous travel at a given location.

Allowances for long stays of three months and more, in German law, are taxable. It is thus important to accurately record all details of business trips to ensure compliant per diem calculation.

Stays at a location lasting three days or more in a week are considered “long stays”. Every such stay at a single location is added until reaching three months, unless interrupted by 28 days or more of being away from said location.

Permanent assignments on mobile facilities such as aircraft, ships and other vehicles are exempt from this rule.

Assignments at different locations for a single employer will also be considered “long stays” if totalling over three months.

The “Supplementary BMF letter on the 2014 travel expense reform” details how the 3-month rule is applied in case a traveller’s assignment location changes.

Any interruption of at least four weeks of a long stay restarts the clock on the three-month period. And this, regardless of the reason for said interruption.

One or two-day stays, even at the same location, do not trigger a 3-month period. An employee can work from an external location for two days a week over the course of nine months and still receive their daily allowance.

Managing compliance with the 3-month rule

Germany regulates maximum per diem rates both for travel within the country and travel abroad and updates them every year. In 2023 , the rates for travel within Germany are as follows:

- 14€ per day for business trips lasting eight to 24 hours. This rate applies for the departure and return days of multi-day trips. It also applies for trips with night work extending over two calendar days (the “midnight regulation”) and is allocated to the day with the longest absence.

- 28€ per day for trips lasting more than 24 hours.

- No per diem for trips totalling under eight hours in a 24-hour period.

There are four ways to avoid falling under the 3-month rule:

- Interrupting the business trip for more than four weeks (whether for work, holidays or an illness).

- Carrying out activities for different customers in the same location during the trip.

- Spending two days per week or less working at the external location.

- Working on a mobile facility such as a ship.

How Mobilexpense ensures compliance with the 3-month rule

The rules, rates and regulations that apply to German organisations are regularly updated in our solution by our Compliance Team. This ensures that entries made by your employees will always be compliant, avoiding miscalculations and saving you, and them, valuable time.

Creating compliant per diem claims is as easy as entering departure and return dates and a destination. Our up-to-date solution runs all the calculations for you based on the data from the BMF.

You may also enjoy

These Related Stories

Updated VAT, Mileage and Allowance Rates for 2024

The Role Of Big Data In Expense Management

The Rise of AI and ML in Expense Management

Future of Expense Management: Emerging Tech Trends

- Accounts Payable Software

- Accounts Receivable Software

- Travel & Expense Management

- Payment Automation

- Cash Flow Management

- Account Payable

- Account Receivable

- Travel & Expense

- Press Release

- Get Started

The Complete Guide to Travel and Expense Management (T&E)

Managing travel and expenses for your company can be a complex task, requiring careful attention to detail and adherence to company policies. As your business grows, so does the need for effective travel and expense management. From ensuring compliance with policy guidelines to optimizing costs, there are many factors to consider to make the process smoother for everyone involved.

In this blog post, we will explore the fundamentals of travel and expense management, offering insights into best practices that can help streamline the process. Whether you’re a small business with a handful of travelers or a large corporation with a global workforce, understanding the basics of travel and expense management is essential for maintaining control over your travel costs and ensuring compliance with your company’s policies.

What is Travel and Expense Management?

Travel and Expense Management (T&E) is the process of overseeing and controlling an organization’s spending on business-related travel and expenses. It involves documenting, processing, and monitoring the expenses to ensure they are in line with company policies and tax regulations.

T&E management includes various tasks such as booking travel arrangements, managing expenses, and ensuring compliance with corporate policies and legal requirements. The goal of travel and expense management is to optimize spending, improve efficiency, and maintain transparency in business expenses.

Key components of travel and expense management include:

- Approving travel requests

- Booking travel arrangements (such as flights and hotels)

- Managing corporate credit cards

- Submitting and approving expense claims

- Handling reimbursement

- Auditing expenses for compliance

- Guiding travel policies to employees

T&E management helps organizations save money, time, and resources by providing visibility into spending patterns and ensuring that employees only spend money on necessary expenses during business trips. It plays a crucial role in maintaining accurate financial records and ensuring compliance with tax regulations .

What is the Travel & Expense Policy?

A travel and expense policy is a set of guidelines and rules established by a company to regulate how employees spend company funds on business trips and related expenses.

These policies typically cover various aspects of travel and expenses, including:

- How and where to book travel

- Criteria for approving or rejecting travel itineraries

- Expense reimbursement process

- Guidelines for flights, trains, and class accommodations

- Approved hotels and allowable incidental expenses

- Ground transportation guidelines

- Meal allowances

T&E policies are designed to ensure that employees understand the company’s expectations regarding travel and expenses and to provide clarity and consistency in how these expenses are managed and reimbursed. They help companies control costs, ensure compliance with regulations, and provide employees with clear guidelines for managing expenses while traveling for business.

Why is Travel and Expense Management Important?

Travel and expense management is essential for controlling costs, ensuring compliance, optimizing processes, and enhancing employee satisfaction. Implementing an effective travel and expense management process can lead to significant cost savings and operational efficiencies for businesses of all sizes. Let’s take a look at the importance of T&E management:

- Cost Control: Effective management of travel and expenses helps control costs by ensuring that expenditures are in line with budgets and company policies. It allows businesses to identify areas of overspending and implement measures to reduce unnecessary expenses.

- Compliance: Compliance with company policies and regulatory requirements is crucial. A proper travel and expense management process helps ensure that expenses are incurred for legitimate business purposes and comply with tax regulations , reducing the risk of audits and penalties.

- Visibility and Reporting: A centralized process provides visibility into travel and expense data, allowing businesses to track spending, analyze trends, and generate reports. This visibility helps in making informed decisions and optimizing travel budgets.

- Streamlined Processes: Managing travel and expenses manually can be time-consuming and prone to errors. An automated system streamlines processes, reducing administrative burden, and improving efficiency.

- Policy Enforcement: A robust travel and expense management system helps enforce company policies related to travel and expenses. It ensures that employees adhere to guidelines regarding travel bookings, expense submissions, and reimbursement , promoting accountability and compliance.

- Employee Satisfaction: A well-managed travel and expense process can enhance employee satisfaction by providing a smooth and timely reimbursement process. It also ensures that employees are aware of the company’s travel policies and procedures, reducing confusion and frustration.

What are the Stages of Travel and Expense Management?

Here is a breakdown of the eight different stages of travel and expense management:

1. Developing an Expense Policy

Develop a comprehensive expense policy that covers all aspects of travel and expense management. Specify allowable expenses, limits, and procedures for requesting funds, making authorized transactions, submitting expense reports, and receiving reimbursements. Include clear guidelines for travel-related expenses to ensure consistency and compliance.

2. Streamlining Pre-Travel Processes

Use travel and expense management automation platforms to simplify the pre-travel process. These platforms enable employees to submit travel requests, which are then routed to managers for approval. Managers can quickly review and approve requests, and employees can book their travel directly through the platform, ensuring all bookings are recorded and tracked efficiently.

3. Managing Expense Incurrence

During business trips, employees will incur various expenses, such as meals, transportation, and accommodation. Companies can provide employees with cash advances, and corporate credit cards, or require them to pay out of pocket and submit expense reports for reimbursement. Clear communication and guidelines are essential to ensure employees understand the process and comply with company policies.

4. Efficient Receipt Handling

Managing receipts is a crucial aspect of expense management. Traditionally, employees would need to keep track of paper receipts and submit them along with their expense reports. However, digital solutions offer a more convenient option. Employees can use mobile apps to capture and upload receipts, which are then stored securely in the cloud. Some platforms even offer OCR capabilities, automatically extracting relevant information from receipts and eliminating manual data entry.

5. Standardizing Expense Reporting

Standardize the expense reporting process to ensure consistency and accuracy. Provide employees with easy-to-use tools, such as mobile apps or web-based forms, to submit their expense reports. Include prompts for required information, such as date, amount, and purpose of the expense, to streamline the reporting process and minimize errors.

6. Implementing an Approval Process

Implement a clear and efficient approval process for expense claims. Use expense management software to automate the workflow, allowing managers to review and approve claims quickly. Ensure that all claims are reviewed for compliance with company policies before approval to prevent unauthorized expenses.

7. Ensuring Prompt Reimbursement

Prompt reimbursement of expenses is essential to maintain employee satisfaction. Once expense claims are approved, ensure that reimbursements are processed promptly. Consider using direct deposit or other electronic payment methods to expedite the reimbursement process and reduce administrative burden.

8. Conducting Compliance Audits

Regularly audit expense reports to ensure compliance with company policies and regulations. Look for any anomalies or discrepancies that may indicate fraudulent activity. Conducting regular audits helps maintain the integrity of the expense management process and identifies areas for improvement.

What are the Challenges of Travel and Expense Management?

Managing travel and expenses poses several challenges for organizations, ranging from tracking and controlling costs to ensuring policy compliance. These challenges can impact financial health, employee satisfaction, and operational efficiency. Understanding these challenges is crucial for implementing effective solutions. Here are some common challenges of travel and expense management:

1. Trouble with Policy Compliance

A common challenge in managing travel and expenses is the lack of enforcement of policies. This often occurs due to unclear policies. When policies are ambiguous, employees may spend without regard to guidelines, leading to uncontrolled expenses and budget strain.

As businesses grow, ensuring compliance becomes more challenging. Unauthorized bookings and other policy breaches can occur due to various reasons, such as lack of awareness or attempts at internal fraud.

2. Lack of Data Management

Even with enforced expense reporting within your travel and expense management policy, there’s always a risk of misplacing receipts and losing travel documents. Ensuring comprehensive tracking of every expense can be challenging, especially when employees have to hold onto receipts until they return home to submit them.

3. Limited Visibility into Spends

One of the significant challenges in travel expense management is the lack of visibility into spending. This often occurs due to ineffective tracking of employee expenditures. Without clear visibility, it becomes challenging to control costs effectively.

While some savings might be possible, a comprehensive understanding of spending or potential savings opportunities remains unclear. Delayed submission of expense reports further complicates the situation, as neither managers nor travelers can accurately assess whether expenses align with budgetary constraints.

4. Unclear Expense Policies

Corporate travel and expense management involve many considerations, making it easy to overlook aspects when creating your expense policy. This can create confusion and ambiguity, leading to a lack of clarity for employees.

5. Complicated Expense Workflows

Managing business travel expenses often involves navigating complex workflows. Obtaining approvals from multiple stakeholders can be time-consuming, especially when quick payments are needed. Additionally, the process of filing expense reports after a trip can involve many complex steps.

6. Labor-Intensive Manual Processes and Paperwork

Many businesses use manual processes, such as spreadsheets, to track their expenses. While this may seem efficient initially, it becomes difficult to manage as the business grows. Manually inputting data into spreadsheets is time-consuming and prone to errors.

Without automation, your team will spend a lot of time on manual data entry and paperwork. It includes collecting and storing receipts, as well as entering each transaction from business trips into spreadsheets. These tasks can decrease productivity and lead to inefficiencies.

7. Expense Fraud

Expense fraud can pose a significant threat to your company’s finances, as employees may misuse company funds by submitting false expenses or using them for personal trips. To prevent such fraud, organizations must implement measures to detect and prevent fraudulent activities.

Expense fraud can take various forms, including internal fraud where employees intentionally make unauthorized transactions, or external fraud where criminals steal company funds. Not enforcing travel and expense policies or carefully controlling spending can lead to multiple fraud attempts, some of which may go unnoticed.

8. Difficulty Managing Multi-Currency Expenses

Business travel can involve transactions in different currencies, which can be complex. Managing expenses in foreign currencies requires decisions on when to convert rates, such as at the time of purchase or reimbursement.

9. Challenges with Filing Expense Reports

Filing expense reports manually can be time-consuming and tedious. Employees often find it challenging to keep track of receipts and complete the paperwork accurately and promptly. This manual process can lead to delays in reimbursement and create a frustrating experience for employees.

10. Dealing with Reimbursements

Managing reimbursements for employee travel expenses can be challenging. Without an efficient system in place, employees may experience delays in receiving their reimbursement checks, leading to frustration and dissatisfaction. Delayed reimbursements can also impact employee morale and may create financial burdens for employees who rely on timely reimbursements.

Best Practices for Travel and Expense Management

Effective travel and expense management is crucial for organizations to control costs, ensure policy compliance, and streamline processes. Here are some best practices to improve your travel and expense management:

1. Enhance Spend Visibility

Utilizing automated travel expense software and mobile tracking apps allows companies to gain real-time insights into their spending. These tools provide detailed reports on expenses, highlighting areas where costs can be optimized. By having a 360-degree view of expenses, businesses can make informed decisions, identify trends, and ensure compliance with policies. Additionally, these tools can help detect any unauthorized or non-compliant spending, allowing for prompt action to be taken. Overall, enhanced spending visibility leads to better financial management and cost control.

2. Prioritize Employee Experience

Improving the travel experience for employees can lead to higher compliance with travel policies. Offering self-booking tools and user-friendly interfaces can make the travel booking process more efficient and enjoyable for employees. This can result in higher employee satisfaction and increased productivity. By prioritizing employee experience, companies can create a positive work environment and improve overall employee morale.

3. Offer Convenient Payment Options

Providing corporate credit cards to employees for business expenses can streamline the payment process and eliminate the need for employees to use personal funds. It can reduce the administrative burden associated with expense reimbursement and ensure that employees are not out of pocket for business expenses. Alternatively, engaging a travel management company can simplify the payment process by consolidating all travel expenses into a single invoice, making it easier to track and manage expenses.

4. Embrace Paperless Processes

Digitizing expense filing and reimbursement procedures can significantly reduce the time and effort required to process expenses. By eliminating paperwork, companies can streamline their expense management processes, reduce the risk of errors, and improve efficiency. Additionally, digital processes can provide greater transparency and visibility into expenses, making it easier for companies to track and monitor spending. Overall, embracing paperless processes can lead to cost savings and improved productivity.

5. Optimize Approval Workflows

Designing workflows that facilitate quick approval for essential expenses can expedite the expense approval process. By setting up auto-approval for certain spending categories, companies can reduce the time and effort required to process expenses. This can lead to faster reimbursement for employees and improved cash flow for the company. Additionally, optimizing approval workflows can help prevent delays and bottlenecks in the approval process, ensuring that expenses are approved on time.

6. Utilize Travel Expense Policy Templates

Using pre-designed policy templates simplifies the creation of travel expense policies. These templates are often customizable, allowing companies to tailor them to their specific needs and requirements. By using templates, companies can save time and effort in developing policies from scratch. Additionally, templates ensure that policies are comprehensive and cover all necessary aspects of travel expenses. This helps to reduce the risk of misunderstandings and ensures that employees are aware of and comply with the company’s policies.

7. Implement a Paperless Policy

Integrating the travel and expense policy into digital tools makes it easily accessible to employees. This eliminates the need for physical documents, reducing paper waste and simplifying document management. A paperless policy also allows for real-time updates and changes to the policy, ensuring that employees always have access to the most up-to-date information. Additionally, a digital policy can be easily distributed to employees, ensuring that everyone is aware of and understands the policy.

8. Regularly Update Your Policy

Keeping the travel and expense policy current reflects changes in business needs and employee behaviors. Regular updates ensure that the policy remains relevant and effective in managing expenses. This helps prevent misunderstandings and ensures that employees are aware of any changes to the policy. Regular updates also demonstrate a commitment to compliance and best practices in travel and expense management.

Closing Thoughts

Implementing best practices for travel and expense management is essential for organizations to achieve greater efficiency, compliance, and cost control. By enhancing spend visibility, prioritizing employee experience, offering convenient payment options, embracing paperless processes, and optimizing approval workflows, businesses can streamline their travel and expense processes and drive better outcomes.

At Peakflo, we understand the importance of effective travel and expense management. Our Travel and Expense solution is designed to simplify and streamline the entire process. With Peakflo’s intuitive software, organizations can automate expense tracking, simplify reimbursement processes, and gain real-time insights into spending patterns. By leveraging our solution, businesses can optimize their travel and expense management, reduce administrative burden, and ensure compliance with policies, ultimately driving greater efficiency and cost savings.

Mastering Corporate Travel Policy: Best Practices for Creation and Implementation

The ultimate guide to travel requests: streamlining your business travel process, travel allowance: a guide to enhance employee experience, latest post, ditching legacy systems: the key to a sustainable finance landscape, split payment: streamlining transactions for marketplaces, future-proofing b2b payments: the payment automation handbook, what is the accounting cycle 8 steps explained, uplevelling finance operations with rpa adoption.

- Accounts Payable

- Accounts Receivable

- Travel and Expense Management

- B2B Payment Software

- Invoice Management

- Procurement Software

- Product Tour

- Saving Calculator

© 2023 by Peakflo. All rights reserved.

What's an Expense Report? [Why It Matters + Template]

Published: March 30, 2022

If you travel for business – or use a personal vehicle for work — chances are you're incurring some business expenses.

In order to be fairly reimbursed, you need to keep track of expenses in an expense report. On the flip side, employers need expense reports to know how much the business is spending and where.

Here, we'll cover the basics of an expense report, how to fill it in, and see an example in action.

What Is An Expense Report?

An expense report tracks items and services that you purchase while working. These are often — but not exclusively — used for business travel.

Although an expense report is necessary for any employee who wants to be reimbursed for a business expense — like travel, gas, or meals — they're equally important for the employer. Here's why:

1. Accurate reimbursements.

Here's the rub — employees want reimbursement for the expenses they've paid out-of-pocket. But, on the flip side, employers want assurance that these expenses are fair and legitimate. An expense report provides a standardized process that addresses both these concerns.

2. Cost control

Expense reports allow you to track spending over time and identify whether any particular expense category (such as transportation or hotels) is driving costs excessively. Then, you can strategize how to reduce or eliminate these costs.

3. Simplifies tax deductions

Many business expenses are tax-deductible. However, you need to accurately record them (with receipts) before claiming a deduction. This is where expense reports can come in handy — providing solid evidence about when, where, and how expenses were incurred.

Now let's cover what to include in an expense report and popular business categories.

What to Include in an Expense Report

An expense report contains a variety of information — however, there are several details you must include, such as the:

- Identifying information of the person filling out the report — this could be your name, designation, or contact info.

- Date - the date on which you incurred the expense.

- Amount - the total cost of an expense incurred, including taxes.

- Description – a brief account of each business expense.

- Category - the type of expense incurred (e.g. parking, office supplies, or gas).

A report may also include nice-to-have information, like whether an expense belongs to a specific client or project, or space to explain certain expenditures that don’t fit clearly into a category.

Next, you must calculate (and record) the subtotal for each expense category and the grand total of all expenses.

Expense Report Template

Download this template

Common Expense Report Categories

With expense categories, you will better understand what expenses can and cannot be reimbursed. Plus, you’ll also alleviate future headaches for your bookkeeper or tax preparer.

Speaking of taxes, it's a good idea to use the IRS' categories in your expense report. Here's a list of the most common types:

- Car and truck expenses

- Commissions

- Legal and professional services

- Membership fees

- Office supplies

- Postage and shipping

- Repairs and maintenance

- Transportation

- Travel expenses (hotels, meals, parking, etc.)

- Vehicles, machinery, and equipment

Choosing the right categories will depend on your type of business. For example, a drop-shipping company will dedicate categories for shipping, printing, and storage, whereas an advertising firm may have categories for digital services.

How to Fill Out an Expense Report

An expense report can either be filled manually or electronically using accounting software or apps.

Let's first discuss how to fill out an expense report manually:

- Start by filling out the mandatory information in the report — such as your name and designation.

- In chronological order, list each expense under the appropriate category.

- Along with each expense, include the date it was incurred, the total amount, and a brief description of it.

- Calculate the subtotal for each category and the grand total of all expenses.

- Finally, attach corresponding receipts to the report. The receipts should clearly show the date and total amount.

- Submit the report to your line or department manager who will check it for illegitimate claims or policy violations.

Many small businesses can benefit from using a standard expense report template. However, depending on your size or industry, it could make sense to use accounting software — like Xero , QuickBooks , or FreshBooks — to keep track of expenses.

Further, bookkeeping apps like Sunrise , ZoHo Books , GoDaddy Bookkeeping make it easy for employees to capture receipts, car mileage, and other expenses on the go. Or for businesses looking for complete control expense management software such as ExpenseOnDemand .

Final Thoughts

Expense reports take the guesswork out of how much money your business is spending and where it's going. Done correctly, you can accurately reimburse employees, simplify your taxes, and even make financial projections for the coming year.

Don't forget to share this post!

Related articles.

Accounting 101: Accounting Basics for Beginners to Learn

How To Conduct a Small-Business Valuation

A Guide to Managerial Accounting

What Is Goodwill in Accounting: An Explainer

A Quick Guide to GAAP Accounting for Your Business

How To Do Accounting for Your Startup: Steps, Tips, and Tools

Gross Revenue vs. Net Revenue: An Explainer

![The Plain-English Guide to Revenue Run Rate [Infographic]](https://blog.hubspot.com/hubfs/run-rate.jpg "travel expense report deutsch")

The Plain-English Guide to Revenue Run Rate [Infographic]

The Beginner's Guide to Balance Sheets

What Is a Profit and Loss Statement?

Track your work expenditures to get reimbursed appropriately.

Powerful and easy-to-use sales software that drives productivity, enables customer connection, and supports growing sales orgs

- [email protected]

Home » Hot Topics » Germany per diem rates and how to manage employees travel expenses

Germany per diem rates and how to manage employees travel expenses

- 3 September 2022

One of the most frequently asked questions we get asked by our clients is how to manage employees travel expenses and Germany per diem rates. German regulations governing per diems, telecom expenses, hotel costs, meals reimbursements, mileage and so on, can often be confusing and different from an organization’s home-country rules.

Companies setting up shop in Germany are understandably concerned about how challenging it can be to stay compliant with German tax laws and want to avoid fines and reputational damage.

For this reason, we have decided to write this article with the aim of providing not only an overview on German travel expense reimbursements (as part of good expatriate management best practices ) but also to dissect and explain some of the finer details surrourding the complex circumstances companies face.

What are per diem rates?

According to Investopedia.com per diems (in German “ Tagespauschalen ”), from the Latin for “ by the day ”, refers to daily allowances paid to employees to cover costs incurred while on a business trip.

More specifically, the law in Germany talks about a lump sum for meals being paid to an individual as compensation for the expenses incurred in working outside their home and main workplace.

Moreover, an employment contract (or any other company issued policy) or collective bargaining agreement may also stipulate that per diems are to be used to reimburse employees.

Tax repercussions are likely (although as we will discuss in this article, not for all expenses categories) if employers choose to reimburse employees for actual expenses above the permitted per diem’s allowance instead.

On the other hand, there is less of an administrative burden for both companies and their employees when sticking with per diem rates as there is no need to:

– submit an itemized claim

– attach accompanying receipts

– update per diem rates each year in line the rising cost of living (the German Finance Ministry takes care of it)

What is not covered by Germany per diem rates

Now that we have a per diem definition and a law clarifying what per diem allowances are meant to cover in Germany, let us briefly look at what type of travel expenses, per diems are not meant to cover:

- Air fares

- Transport to and from the airport and/or meetings

- Hotel costs for staying overnight

- Breakfast, lunch and/or dinner whilst meeting clients

These types of expenses should be in fact be claimed as part of a separate expenses claim request (a template is provided towards the bottom of this article) for actual travel expenses incurred.

Per diem rates within Germany

When employees are traveling on business within Germany the costs of subsistence (drinks and meals) is typically reimbursed according to the applicable per diem rates which currently are:

– between 8-24 hours, 14 EUR

– for a full 24 hours day, 28 EUR

For the first and last day of travel, the applicable per diem rate is always 14 EUR.

Furthermore, there is also an overnight allowance of 20 EUR for accommodation.

In practice though, only self-employed individuals tend to claim this allowance via their German tax return as accommodation is usually fully paid by the employer for travelling employees.

Conditions for eligibility of per diem allowances

We have already discussed above what is not covered by per diem allowance.

Let us now look more specifically at what are some of the conditions to be fulfilled for employees to be eligible to claim the above mentioned per diem rates in full.

The main condition is that the full per diem meal allowances will only be paid if the employee actually covers the costs of their own food .

In the case of meals that the employee took and that are included for example in a hotel invoices (breakfast, lunch, dinner) or that the employer provided, there will be a compulsory reduction of the lump sum amount entitlement as follows:

– 20% reduction if breakfast is already included in hotel invoice

– 40% reduction if lunch / dinner are already provided by the employer.

It is also worth mentioning that meals provided by the employer for trips shorter than 8 hours are treated as fringe benefits and thus taxable on the employee are the following nominal values:

– breakfast, 1.77 EUR

– lunch or dinner, 3.30 EUR

Other conditions / rules attached to the eligibility for per diem rates in Germany include:

– hours can be added together for multiple trips within the same day

– The tax-free reimbursement can only be for 3 continuous months of business travel. These 3 months can then be reset after a 4 weeks break

– All expense invoices should be addressed to the company’s corporate address and if they exceed 150 EUR, they should state the VAT amount

Per diems outside of Germany

Considering that the cost of living between countries (and sometimes even between cities within the same country) can vary significantly, the German Ministry of Finance each year publishes a table with the up to date international per diem rates.

However, due to the Covid pandemic, the international per diem and overnight allowances issued by virtue of the German Federal Travel Expenses Act, have not been updated on January 1, 2022.

As a result, the tax-free per diem lump sums published by the BMF letter dated 3 December 2020 , on “Tax treatment of travel expenses and travel expense allowances for business and professional trips abroad from January 1, 2021” – Federal Tax Gazette Part I (BStBl I) page 1256, are also valid for the calendar year 2022.

Overview of other travel expense reimbursements in Germany

Entertainment.

Entertainment expenses for events in which only employees working for the same company took part are not accepted as an external party also needs to be involved.

Additionally, invoices for entertainment expenses reimbursements should clearly show the following information:

- Employee/s name/s

- Name/s of the people entertained

- The reason for the entertainment provided

- The place, date and signature

0.30 EUR/Km can be reimbursed tax-free. The lump sum rate covers all expenses related to the car such as insurance, depreciation, petrol / diesel, maintenance, car wash, etc.

Tax-free reimbursements for expenses incurred during business use for private cars can only be paid if the employees states on their expenses claims the driven KMs and other relevant details about the trip such as start / end KMs balance, details of the route taken and the reason for the trip.

Anything paid in addition to the 0.30 EUR/KM rate, will be deemed taxable.

This means that the amount will have to be split up in a tax-free part and a taxable part (taxed at individual income progressive tax rates).

Telecom expenses / home office

If the home telephone / mobile phone / internet contracts are between the telecommunication company and the employee and not between the telecommunication company and the employer, there are 4 possibilities to reimburse these expenses:

1) The employer can pay a monthly lump sum of 20% of the invoice amount up to a max. of 20 EUR tax free to the employee. Any additional reimbursements would be taxable.

2) If the employee highlights the costs incurred for the employer on the telecommunication company’s itemized bill every month, the employer can reimburse those costs tax-free.

3) If the employee highlights the costs incurred for the employer on the telecommunication company’s itemized bill for a period of 3 months, a typical percentage of total expenses concerning the employer can be calculated on the overall total bill, which can then be compensated tax free going forward every month. Any additional reimbursements above the calculated percentage apportionment would be taxable.

4) The employees could prove they have two different mobile phones / landline numbers so that they could clearly be differentiated between the one used for business purposes and the one used for private purposes. In such a scenario, all the expenses incurred for business purposes on the dedicated line / number can be reimbursed tax-free.

Hotel costs

Hotel stays during a business trip can be fully reimbursed tax free provided the invoice is addressed to the employer and not to the employee.

Other expenses

Other expenses such as flight, train or bus tickets can all be reimbursed in full tax-free.

Similarly, the following ancillary expenses can also be reimbursed tax-free for the full actual amount incurred:

– Storage of luggage (including luggage insurance)

– Letters to the employer or to business partners / clients

– Parking fees / tolls

– Rental car at the place of the destination

– Damages to the employee’s belongings if they are typical for business traveling